Introducing the 2022 State of Crypto Report

*NEW*: State of Crypto 2023 is now live. Check out the report — or explore web3 adoption, DeFi and NFT activity, and more in our new interactive index.

A lot has changed in the state of crypto since we started investing in the area nearly a decade ago.

This report is the first of what will be an annual overview of trends in the crypto industry, shared through the a16z crypto vantage point of both tracking data and across the countless entrepreneurs and builders we meet. It’s for anyone who seeks to understand the evolution of the internet, and where we are on the journey towards a decentralized, community-owned-and-operated alternative to the centralized tech platforms of web2 – especially as it touches creators and other builders.

The top themes are distilled into five summary takeaways below, but be sure to dig into these 50+ slides (full deck for the 2022 State of Crypto Report available for download below); be sure to also sign up for the a16z crypto newsletter to continue getting insights as well as updates about upcoming resources and to listen to the new web3 with a16z podcast to dive deeper into the findings and methodology.

5 key takeaways

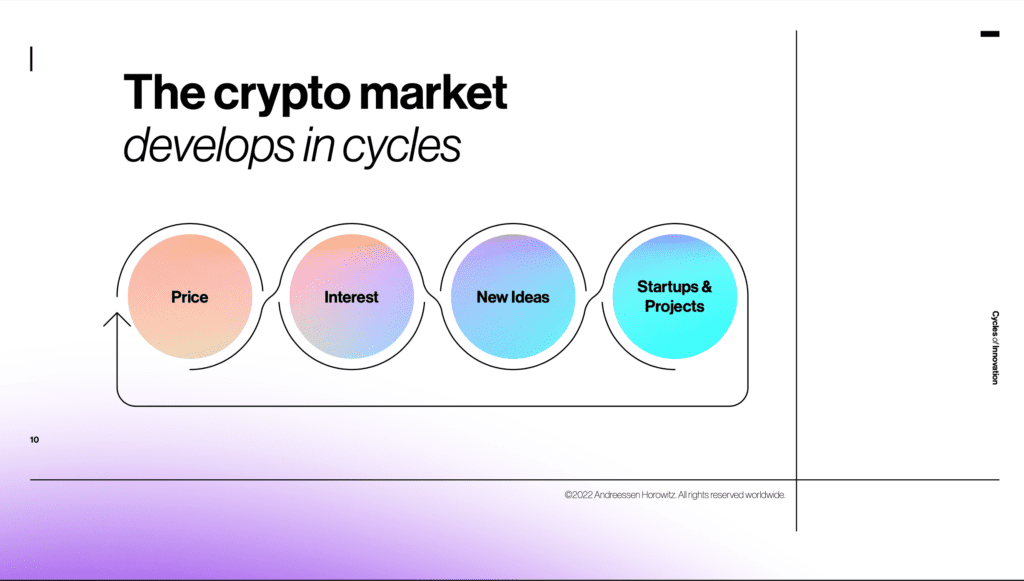

#1 We’re in the middle of the fourth ‘price-innovation’ cycle

Markets are seasonal; crypto is no exception. Summers give way to the chill of winter, and winter thaws in the heat of summer. Advances made by builders during dark days eventually re-trigger optimism when the dust settles. With the recent market downturn, we may be entering such a period now.

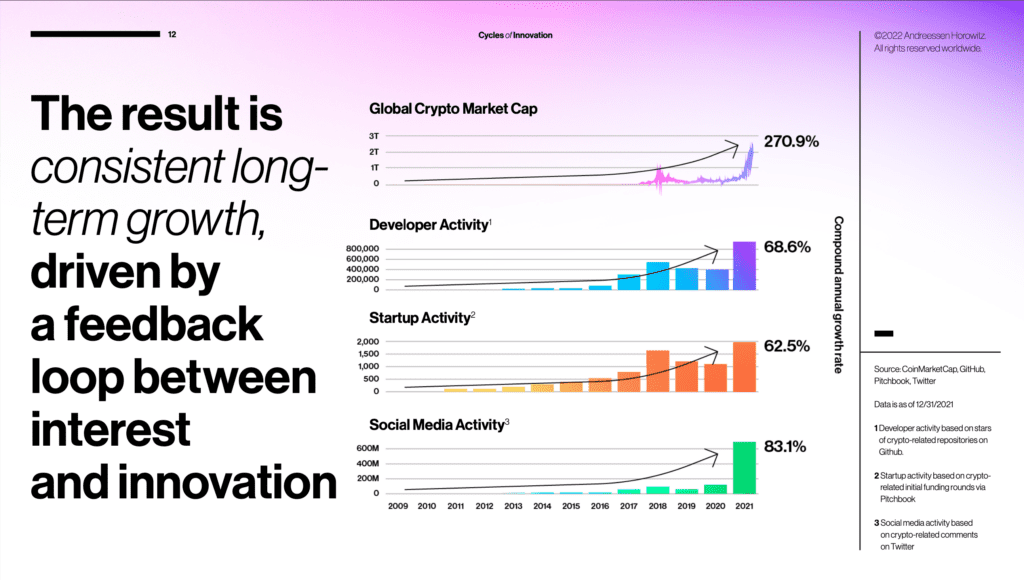

Although crypto can be volatile and its cycles seem chaotic, there is an underlying logic at work, as Chris and Eddy first pointed out in 2020. (See slides 9 through 12 in the deck.) Whereas prices are often a lagging indicator of performance in some industries, in crypto they are a leading indicator. Prices are a hook. The numbers drive interest, which drives ideas and activity, which in turn drives innovation. We call this feedback loop “the price-innovation cycle”, and it has been the engine that has propelled the industry through multiple distinct waves since Bitcoin’s inception in 2009.

As legendary investor Benjamin Graham once allegorized: It’s best to pay no mind to “Mr. Market”, who frequently boomerangs from exuberance and euphoria to despair and depression. To Graham’s wisdom we add an addendum: Better to build. Consider that any prospective founders who swore off tech and the internet in the aftermath of the early-2000s dotcom crash missed the best opportunities of the decade: cloud computing, social networks, online video streaming, smartphones, etc. Now is the time to consider what the equivalent successes will be in web3.

#2 web3 is much, much better for creators than web2

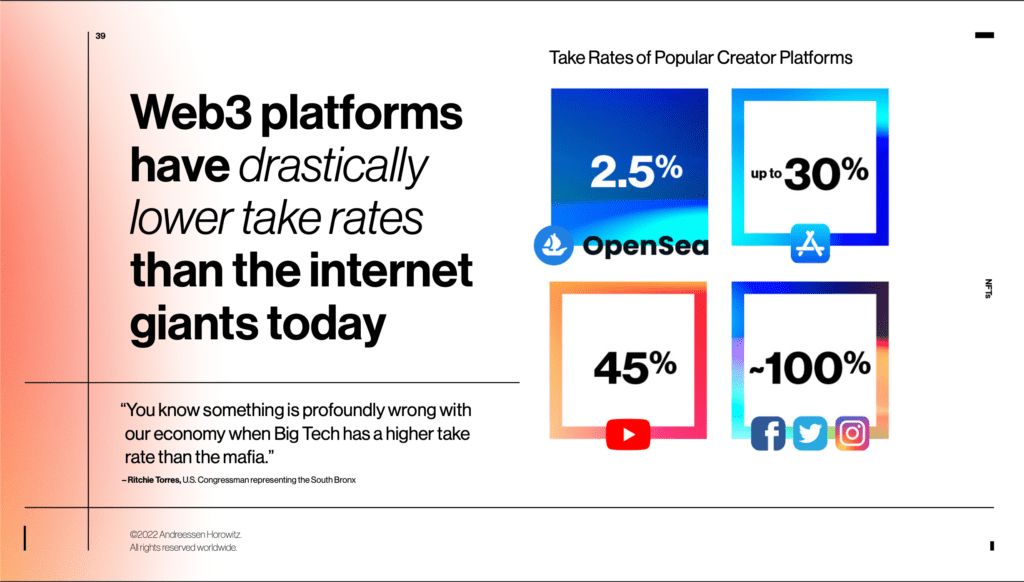

The take-rates of web2 giants are extortionate; web3 platforms offer fairer economic terms. (See slide 39 in the deck.) Compare Meta’s nearly 100% take-rates across Facebook and Instagram to NFT marketplace OpenSea’s 2.5%. As U.S. Congressman Ritchie Torres noted in a recent op-ed, “You know something is profoundly wrong with our economy when Big Tech has a higher take rate than the mafia.”

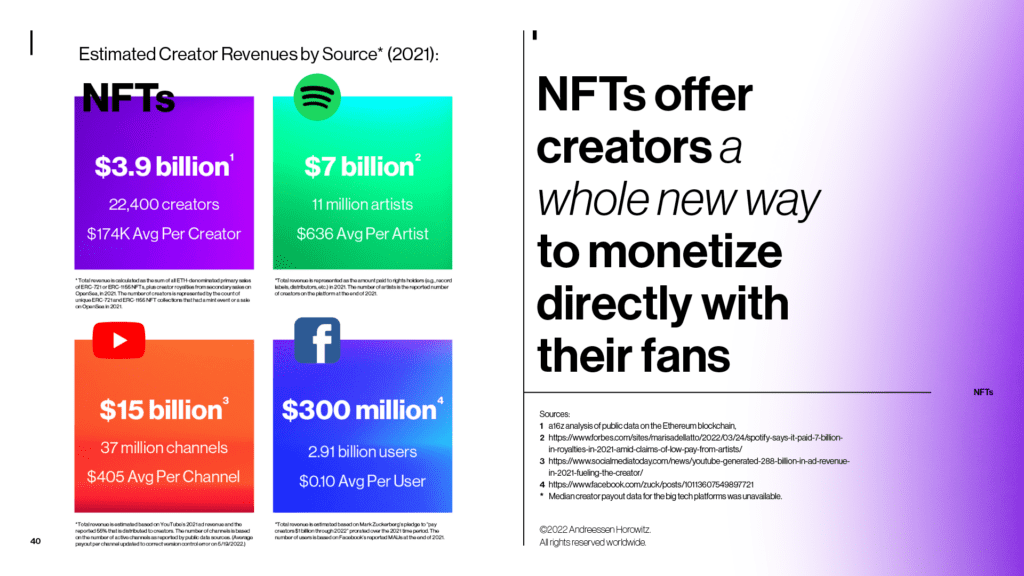

Our team conducted new data analysis to estimate how much web3 is paying out to creators compared to web2. (See slide 40 in the deck.) The numbers are telling even though it’s still early. In 2021, primary sales of Ethereum-based NFTs (ERC-721 and ERC-1155), plus the royalties paid to creators from secondary sales on OpenSea, yielded a total of $3.9 billion. That’s quadruple the $1 billion – less than 1% of revenues – that Meta has earmarked for creators through 2022.

The numbers are even more extraordinary considering how many more web2 versus web3 users there are: We counted 22,400 web3 creators (based on the number of NFT collections) compared to the nearly 3 billion users posting content on Meta platforms. While in absolute terms, Spotify and YouTube paid out more to creators – $7 billion and $15 billion, respectively – the “per capita” disparity is striking. According to our analysis, web3 paid out $174,000 per creator, while Meta paid out $0.10 per user, Spotify paid out $636 per artist, and YouTube paid out $405 per channel. Web3 is tiny but mighty.

#3 Crypto is having a real-world impact

Creator payouts are just one example of crypto’s benefits; there are many others.

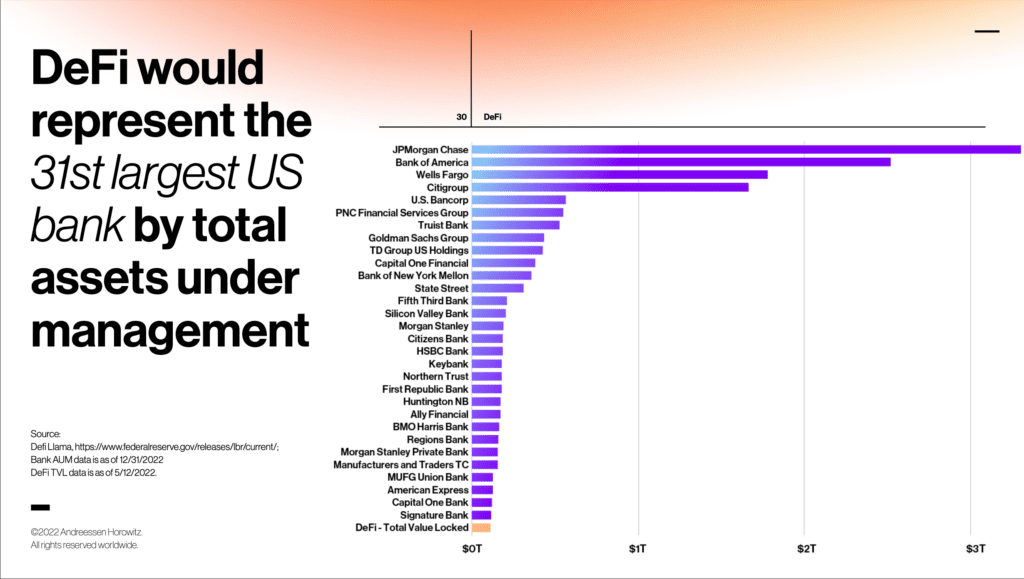

Consider the financial system. The status quo has failed many people: More than 1.7 billion people don’t have bank accounts, per the World Bank. Demand for decentralized finance or DeFi, and digital dollars, has increased dramatically in the past few years, even after accounting for the recent downturn, as the accompanying slides show. (See slides 26, 28, and 33.) For underserved and unbanked populations – 1 billion of whom have mobile phones – crypto offers a shot at financial inclusion. Projects like Goldfinch are expanding access to capital that would otherwise be unavailable in emerging markets.

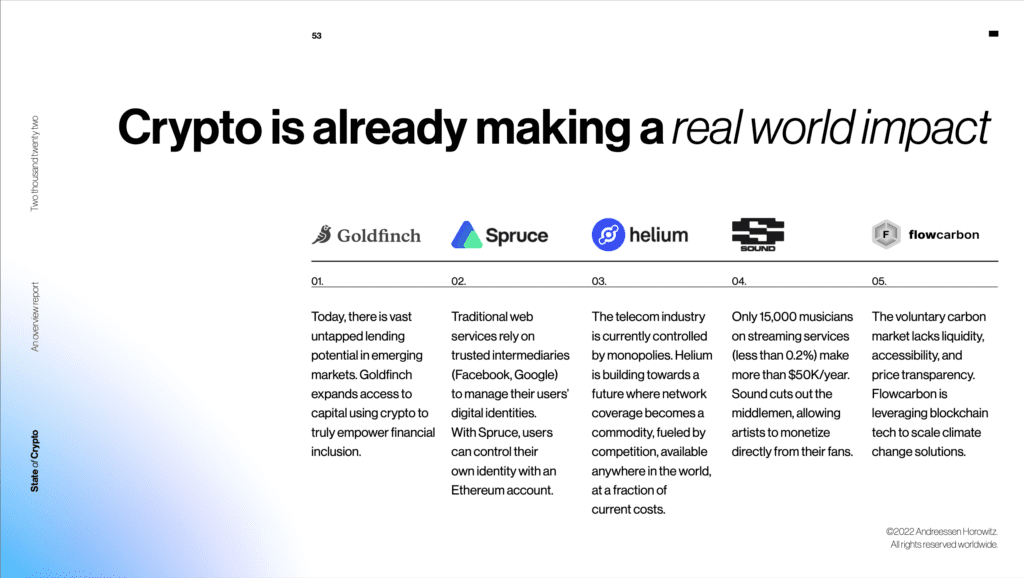

Crypto is addressing other broken marketplaces, too. (See slide 53 in the deck.) Flowcarbon is revamping carbon credits by making these increasingly important units of account transparent and traceable on blockchains. Helium, a grassroots wireless network, is posing the first legitimate, decentralized challenge to entrenched telecom giants. And Spruce is enabling people to control their own identities, rather than ceding that power to online intermediaries, like Google and Meta, who profit off people’s information through their data-mining business models.

The list goes on. DAOs, or decentralized autonomous organizations, show how strangers can coordinate and cooperate economically to achieve goals. NFTs grant people virtual property rights across profile pictures, artworks, music, in-game items, access passes, land in virtual worlds, and other digital goods. And token incentives enable newcomers to bypass the “cold-start” problem and jumpstart network effects. Crypto is far more than just a financial innovation – it’s a social, cultural, and technological one.

We’ve barely just scratched the surface of what’s possible.

4. Ethereum is the clear leader, but faces competition

Ethereum dominates the web3 conversation, but there are plenty of other blockchains now too. Developers of blockchains like Solana, Polygon, BNB Chain, Avalanche, and Fantom are angling for similar success. (See slides 15 and 27 in the deck.)

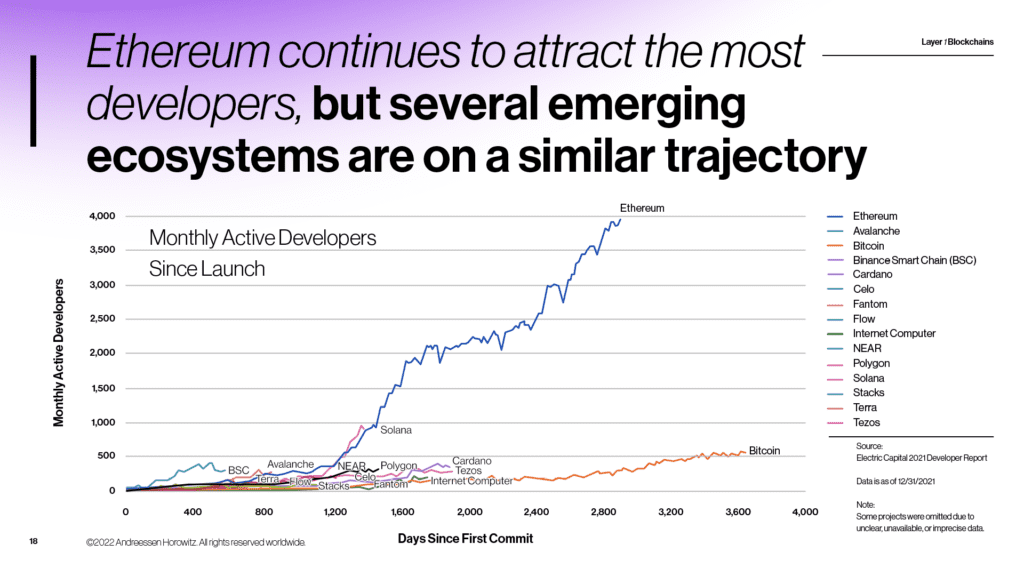

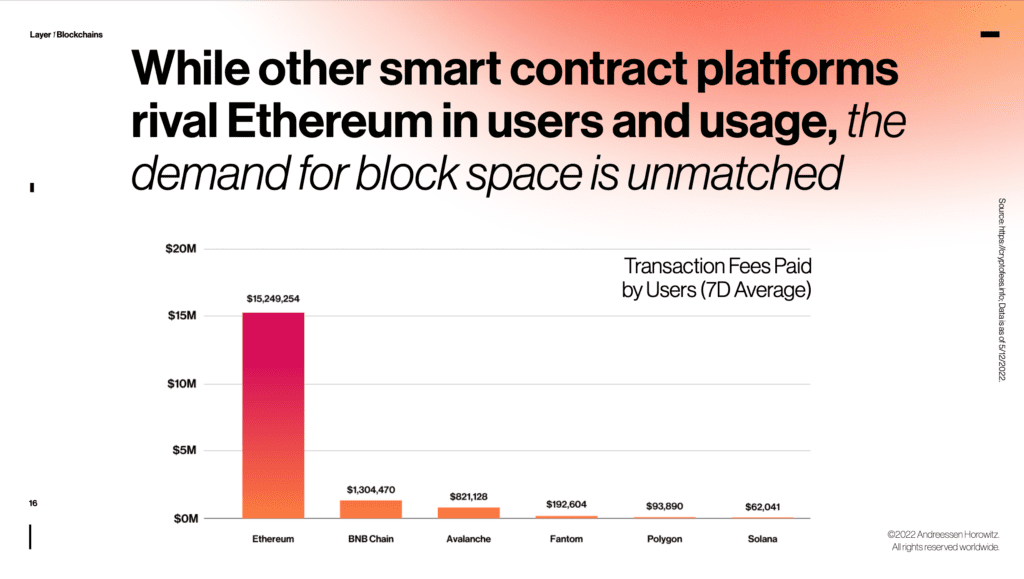

Ethereum’s lead has much to do with its early start, and, the health of its community. As far as developer interest, Ethereum has far and away the most builders, with nearly 4,000 monthly active developers. (See slide 18.) Following that is Solana (with nearly 1,000) and Bitcoin (about 500). Ethereum’s overwhelming mindshare helps explain why its users have been willing to pay more than $15 million in fees per day on average just to use the blockchain – remarkable for such a young project. (See slide 16.)

Ethereum’s popularity is also a double-edged sword. Because Ethereum has historically prized decentralization over scaling, other blockchains have been able to swoop in and attract users with promises of better performance and lower fees. (Some might argue they do so at the expense of security.)

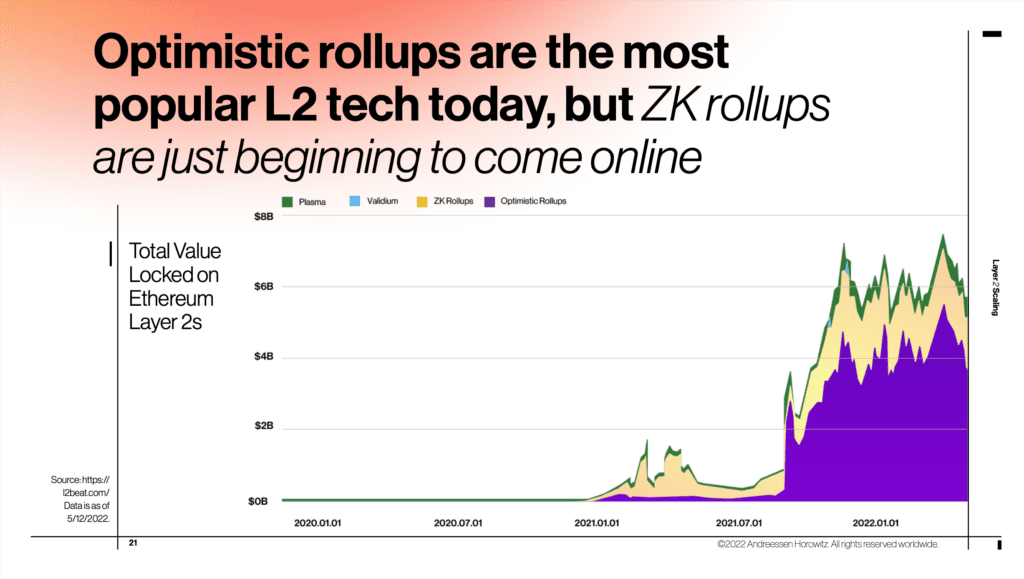

Beyond challenger blockchains, we’re also seeing incredible progress with interoperability, which allows people to “bridge” assets from one blockchain to another, as well as “layer 2” technologies, such as optimistic rollups and zero-knowledge rollups, which aim to lower costs by expanding available blockspace. (See slides 17, and 21 through 23 in the deck.)

Blockchains are the hit product of a new computing wave, just as PCs and broadband were in the ‘90s and 2000s, and as mobile phones were in the last decade. There’s a lot of room for innovation, and we believe there will be multiple winners.

5. Yes, it’s still early

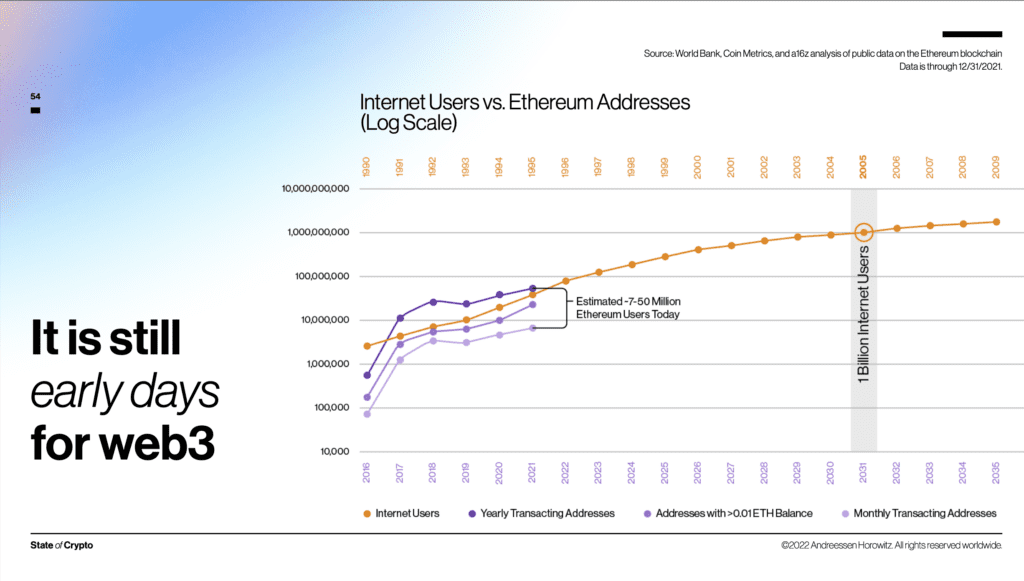

While it’s hard to know the exact number of web3 users, we can reason about the scale of the movement. We estimate there are somewhere between seven million and 50 million active Ethereum users today, based on various on-chain metrics. (See slide 54.) Analogizing to the early commercial internet, that puts us somewhere circa 1995 in terms of development. The internet reached 1 billion users by 2005 – incidentally, right around the time web2 started taking shape amid the founding of future giants such as Facebook and YouTube.

Again, though it’s very hard to estimate, if the trendlines continue as depicted, web3 could reach 1 billion users by 2031. In other words, you’re still early. Much remains to be done. Let’s keep building.

Download the full pdf below, or preview our 2022 State of Crypto Report here:

download a16z crypto’s full 2022 report here

listen to the ‘web3 with a16z’ podcast to dive deeper into data methodology, metrics, FAQs

sign up for the new weekly a16z crypto newsletter here

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investments/.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.