A guide to perpetual futures: How they work and why they're growing so quickly

Perpetual futures (“perps”) are futures contracts that never expire. Once a crypto-native hack, they took off onchain in 2025. They’ve become one of crypto’s biggest markets, covering traditional assets and trillions of dollars in trading volume.

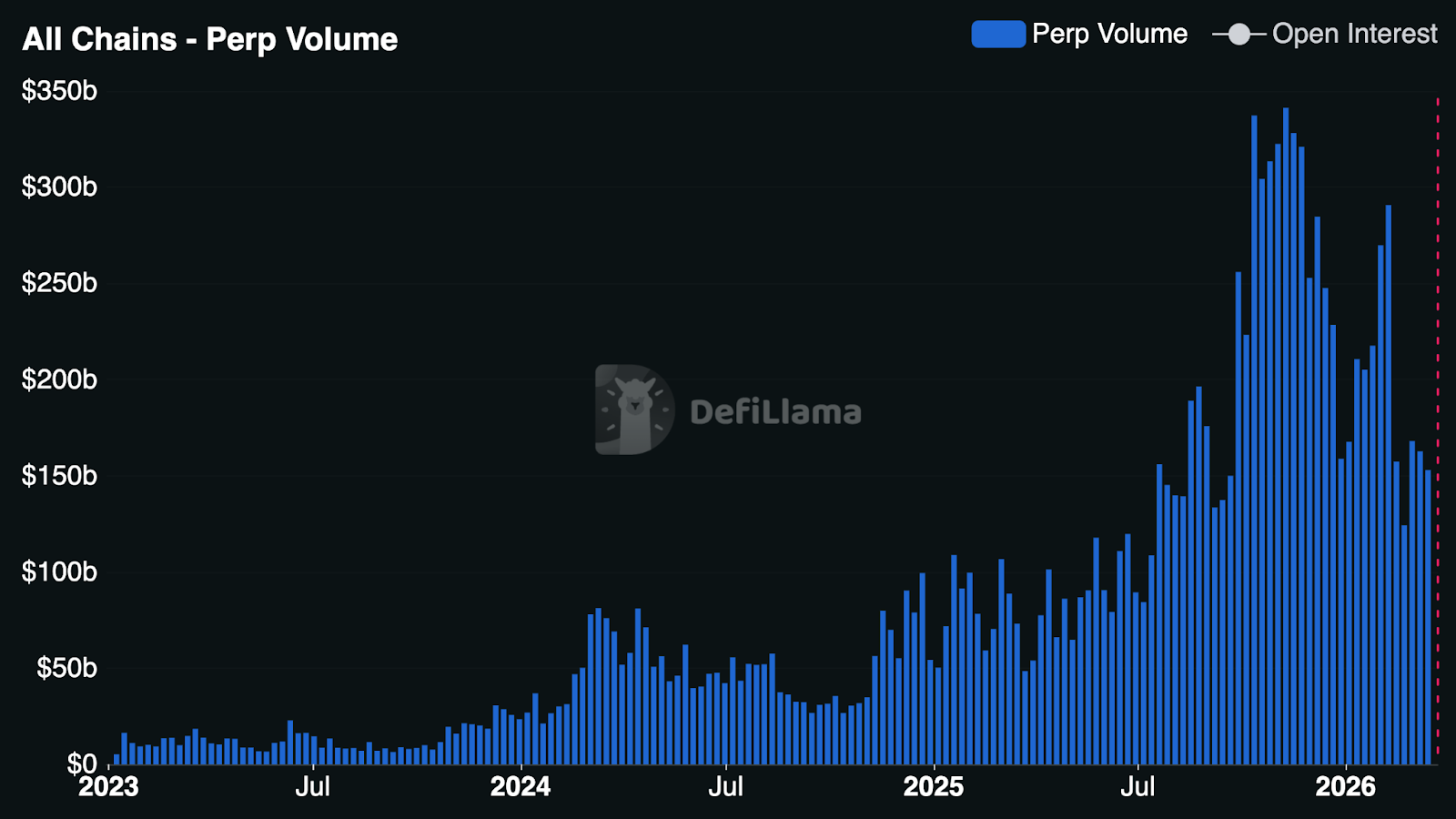

Last year, the top centralized exchanges cleared $86.2T in perp volume (+47% YoY), while onchain perpetuals grew even faster: Leading decentralized exchanges reached $6.7T (+346% YoY). DEX volume now represents roughly 7.8% of CEX volume, up from about 2.5% just a year earlier. [Note: while a small number of U.S.-regulated centralized platforms offer products similar to perpetual futures contracts to U.S. persons, all centralized and decentralized exchanges restrict U.S. persons’ access to true perpetual futures contracts.]

But the bigger story here is that perps are starting to look less like a fringe crypto primitive, and more like a fundamental shift in trading behaviors and market structure.

So what is driving perps’s popularity? And why now? This post looks at why perps are increasingly embraced by traders globally, the scale of the market opportunity, and where builders see opportunity.

A brief history and evolution of perps

The idea itself is actually older than the crypto industry. Perps have existed in theory since 1993, when Nobel Prize-winning economist Robert Shiller introduced the perpetual futures contract, which he originally envisioned as a tool for hedging property-value risks. But perps weren’t popularized in crypto until 2016 with the rise of BitMEX and XBTUSD, the longest-running bitcoin perpetual swap.

A decade later, modern exchanges now offer perpetual futures contracts on equities, indices, commodities, interest rates, startup valuations, and even Nvidia H100 GPU prices.

Perps have been a billion-dollar revenue engine for centralized exchanges for years. As retail appetite for leverage has grown, perps have become a primary venue for short-term price discovery, liquidity, and trading activity — trading multiples more volume than spot on many major Asian centralized exchanges (CEXs).

What’s changed over the last year and a half is that decentralized perp exchanges have started meaningfully eating into centralized exchanges’ share of the perp market. With self-custody as a structural advantage, perp DEXs are rapidly narrowing the gap with CEXs in liquidity, performance, and features for active traders.

With the breakout success of perp DEXs like Hyperliquid, leading crypto wallets and apps rushed to support perps and shipped high-quality trading experiences that made them accessible to millions of users. The latter half of 2025 brought an explosion of perp DEX front-ends — from casual mobile apps to sophisticated, multi-venue trading terminals.

Hyperliquid, in particular, has pushed the boundaries of what DEXs can offer with HIP-3 (Builder-Deployed Perpetuals), a mechanism that allows anyone to permissionlessly launch perp markets on the exchange. With HIP-3, builders can list almost any asset and earn a 50% fee share while managing their own oracles and risk parameters.

At the same time, newer entrants and competitors like Avantis, Lighter, Ostium, and Variational emerged or accelerated product development. More competition forced perp DEXs to differentiate across exchange design, market structure, asset support, and permissionlessness, and helped a few trading venues find strong product-market fit in new categories, like real-world asset (or RWA) perps.

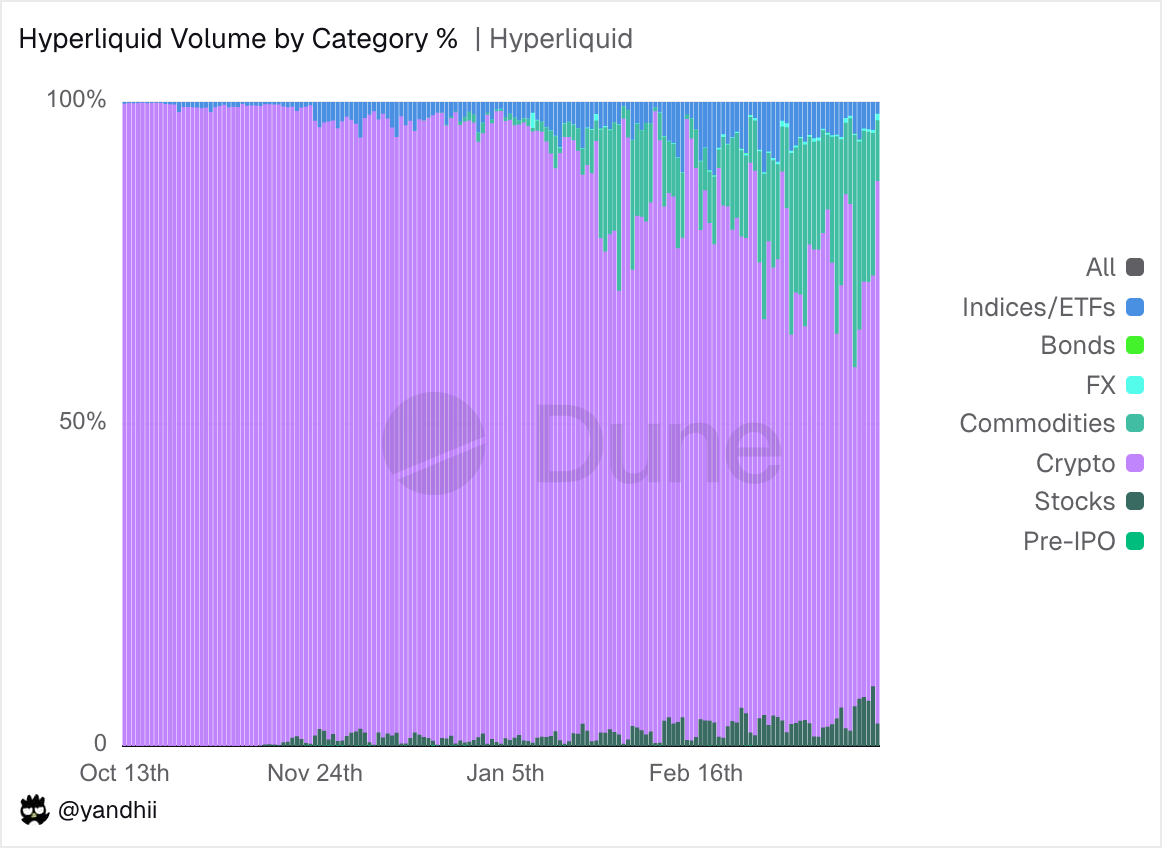

For years, perp traders speculated solely on crypto assets — BTC, ETH, SOL, and a long tail of alts. But late last year, while perp volume largely cooled off from their recent peaks amidst the broader crypto sell-off, RWA perps gained steam. A handful of perp DEXs listed commodities, equities, and equity indices, expanding the universe of tradable assets to include everything from NVDA and Samsung to private companies like SpaceX, as well as commodities like silver and palladium.

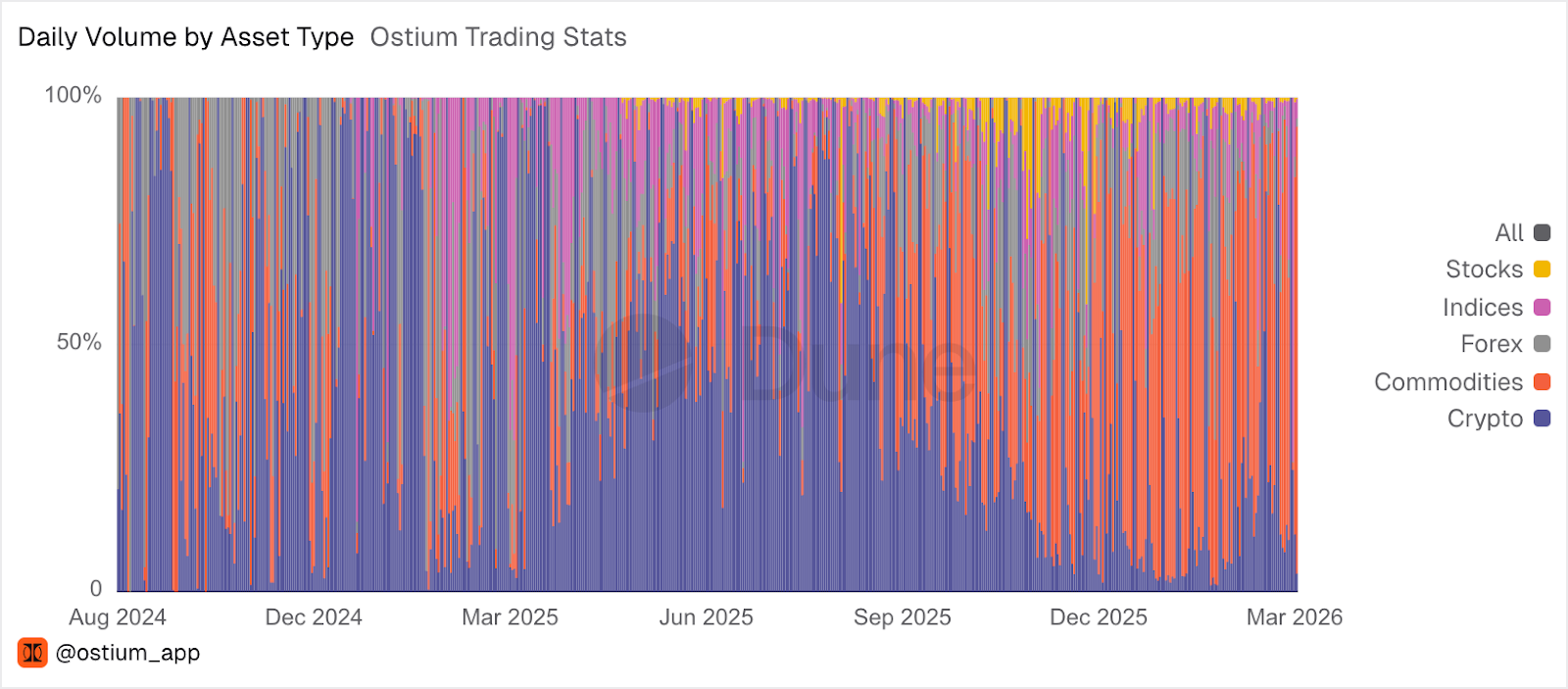

This year, the growth of RWA perps has only accelerated. In recent weeks, RWAs have made up as much as 44% of Hyperliquid’s total volume, and RWA pairs are now consistently among the highest fee-generating pairs on the exchange. On Ostium, RWAs have made up the lion’s share of the exchange’s volume for months.

Decentralized exchanges have also excelled in facilitating price discovery for RWAs like crude oil, especially on the weekends when traditional exchanges are closed.

As RWA perps have taken off, we’ve seen a surge in companies building perps-related products and offerings. The last 6 months alone have brought new exchanges, trading interfaces, market deployers, and liquidity providers.

The players rushing into this category include brand-new startups, startups pivoting toward perps, and some of the largest fintech companies in the world building perp trading into their existing products.

All of these different players are converging on the same opportunity: Perps could become one of the dominant trading instruments in global finance.

The market opportunity for perps

Taking a step back to look at TradFi, options are among the biggest and most actively traded markets on earth. They exist across currencies, equities, indices, commodities, ETFs, and they’re extremely powerful and expressive instruments that enable trading based on many different beliefs: timing, volatility, price ranges, and more.

But when you zoom in on retail trading behavior, a lot of activity is concentrated in one particular options category: short-dated, levered, directional exposure. One prominent example is 0DTE — zero-day-to-expiry options — where traders buy cheap convexity for an intraday move.

This type of trading is one of the fastest-growing options categories. In 2025, average daily volume in 0DTE SPX (S&P 500) options reached 2.3M contracts per day, up 51% year-over-year and representing 59% of total SPX options volume. Several new index products with daily expirations were introduced following this demand, including CBTX and MBTX Bitcoin ETF index options, and options on the equal-weighted Cboe Magnificent 10 index.

So while options have many sophisticated uses — structured hedging, vol trading, dispersion, convexity, etc. — a very large and growing share of retail flow is just looking for short-term, leveraged directional exposure. This type of exposure is exactly the kind of demand perps serve best.

The tradeoff is real: options excel at defined-risk, convex payoffs, and remain the default instrument for volatility expression. The most a trader can lose is their premium. With a perp, the entire collateral position can be liquidated. But for what most retail traders actually want — directional leverage — perps have several structural advantages:

- Always on. The newest generation of perp markets trades 24/7 with no market hours or session gaps. For a global, crypto-native user base, continuous access is the expectation.

- No strikes, no expiries, no rolling. With a single continuous position, traders don’t have to select parameters, manage expirations, or reestablish trades every day or week. They can hold for seconds, months, or theoretically forever.

- Simpler risk surface. With perps, the primary considerations are price, collateral, and liquidation threshold. With options, even if you’re right on direction, you can lose due to theta decay, shifts in implied volatility, and path dependency. Perps strip that complexity away. The trade is directional conviction, expressed cleanly.

- Capital efficiency for sustained exposure. Short-dated options require paying the full premium upfront and rolling repeatedly. Perps require margin — often a small percentage of notional — which is typically more capital efficient for intraday-to-multi-day directional positions.

Options aren’t going away. They have long been a part of financial history and will likely remain dominant for a meaningful portion of trading use cases, especially where defined risk and more complex payoff structures matter. But for the large and growing flow that’s looking for delta-one, directional leverage, perps are already capturing trillions in volume and billions in revenue.

This raises the question: Where in the stack does value accrue as perps move from niche instruments to mainstream trading primitives?

In traditional markets, the most valuable companies were often built around exchange infrastructure, not at the exchange layer itself. For example, Robinhood, a retail broker, commands a higher market cap than Nasdaq, Inc., the exchange Robinhood sits atop.

Whether that pattern holds in crypto — where platforms like Hyperliquid, Lighter, or Ostium are accruing strong enough network effects at the exchange layer — is one of the most interesting open questions in the space.

Either way, builder activity is expanding rapidly. A few areas where we see developer growth:

- Opinionated distribution layers: Vertical or audience-specific front-ends that package narratives, strategies, gamification, or social hooks instead of just presenting markets.

- Market creators and operators (e.g., HIP-3 deployers): Operating a hit market on Hyperliquid allows deployers to essentially own a mini-exchange without having to build the most sophisticated exchange infrastructure. Today’s deployers are likely just scratching the surface of data or price feeds that may be “perpified”.

- Specialized liquidity provision: Market makers that focus on long-tail markets, event-driven books, and cross-venue inventory management.

- Perp-specific data infrastructure: There’s already an emerging ecosystem of community-driven dashboards, block explorers, heat maps, and analytics around positioning, funding rates, liquidations, trader signals, leverage exposure, retention cohorts, and more. More established, high-quality, real-time data makes the entire ecosystem more transparent and efficient for all parties involved.

Of course, there are significant open questions and challenges, ranging across distribution, liquidity depth on newer venues, oracle reliability as the asset universe expands, inevitable edge cases like “10/10,” and regulation, which currently restricts access to these products for U.S. persons. These are expected growing pains as perps graduate from their crypto-native bubble to the main stage of global finance. As the perps ecosystem matures, the question is no longer whether perps will scale; it’s who will build the most valuable applications and infrastructure around them as they do.

Editorial Note: Perpetual futures contracts are currently regulated as derivatives under the U.S. Commodity Exchange Act and may only be offered to U.S. persons through CFTC-registered designated contract markets. As noted above, a small number of U.S.-regulated platforms offer products similar to perpetual futures contracts to U.S. persons, while most centralized exchanges and all decentralized exchanges restrict U.S. persons’ access to such products. The exchanges, platforms, and products discussed in this article—Avantis, BitMEX, Hyperliquid, Lighter, Ostium, and Variational—are not available to U.S. persons.

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investment-list/.

The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures/ for additional important information.