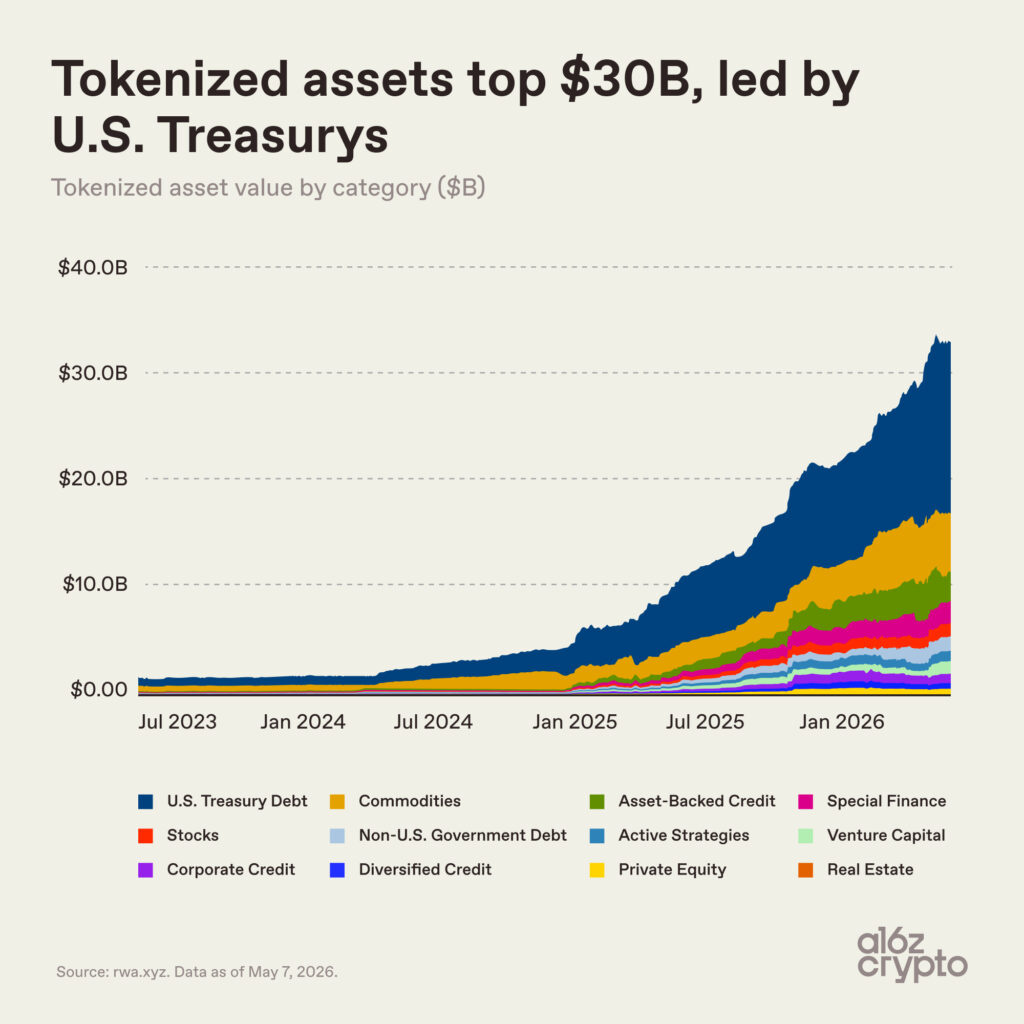

The market for tokenized assets — what others sometimes call “real-world” assets (RWAs) — crossed $30 billion last month. It has since stayed above that level near $34 billion. (And that’s excluding stablecoins.) The market is roughly the size of a regional bank or an elite university endowment; it’s large enough to have an impact, but still tiny relative to all global finance.

As recently as mid-2024, the tokenized assets market amounted to less than $3 billion. Then things accelerated: The GENIUS Act brought clearer stablecoin regulation to the U.S.; institutional onchain infrastructure matured; and a wave of financial institutions moved from blockchain pilots to production systems at roughly the same time. (Stablecoins, though excluded here, fueled growth by making onchain payments and settlement much easier.)

Amid these developments, the market for tokenized assets grew 10x in under two years.

The tokenization take-off

U.S. Treasury debt has driven most of the market’s recent growth.

The appeal is straightforward: Investors can hold a familiar, yield-bearing asset in a faster, more flexible, and digitally native form…while institutions can benefit from more efficient settlement, collateral movement, and integrations with digital markets.

For crypto investors, tokenized Treasurys also provide a way to put idle stablecoins to work while gaining access to traditional money-market yields. BlackRock, Franklin Templeton, and a growing number of asset managers have moved quickly to meet the demand, building a multibillion-dollar market around the idea.

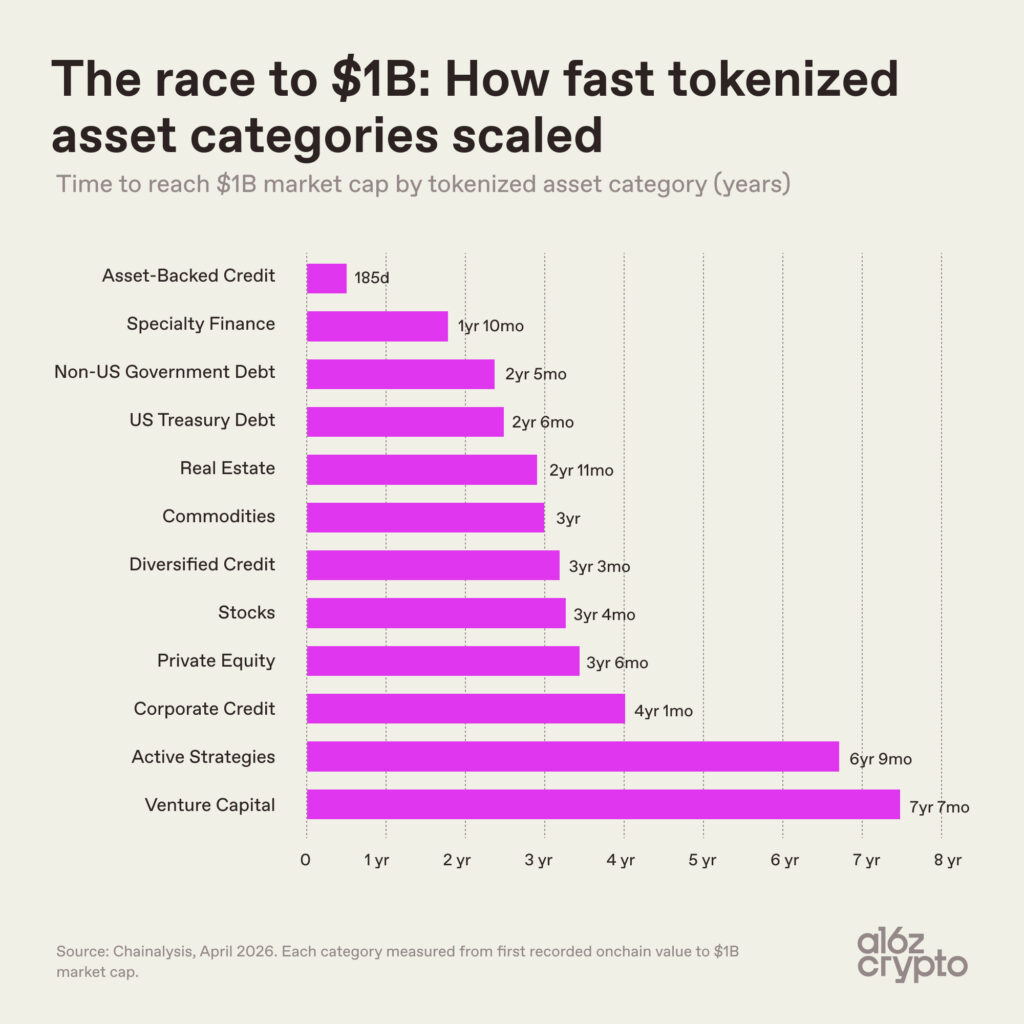

Different categories of tokenized assets have scaled at dramatically different rates, reflecting both the complexity of bringing different asset classes onchain and the speed with which early products have found demand.

Asset-backed credit — including tokenized home equity lines of credit (HELOCs) and lending vault tokens — hit $1 billion in market cap just 185 days after its first recorded onchain activity, the fastest of any tokenized asset category by a wide margin.

Specialty finance — such as tokenized reinsurance contracts and bitcoin mining notes — was the second fastest, crossing the same threshold in under two years.

At the other end of the spectrum, venture capital took more than seven years to reach $1 billion, while active strategies took nearly as long — a reflection of more complex structures, longer time horizons, and greater operational and regulatory complexity.

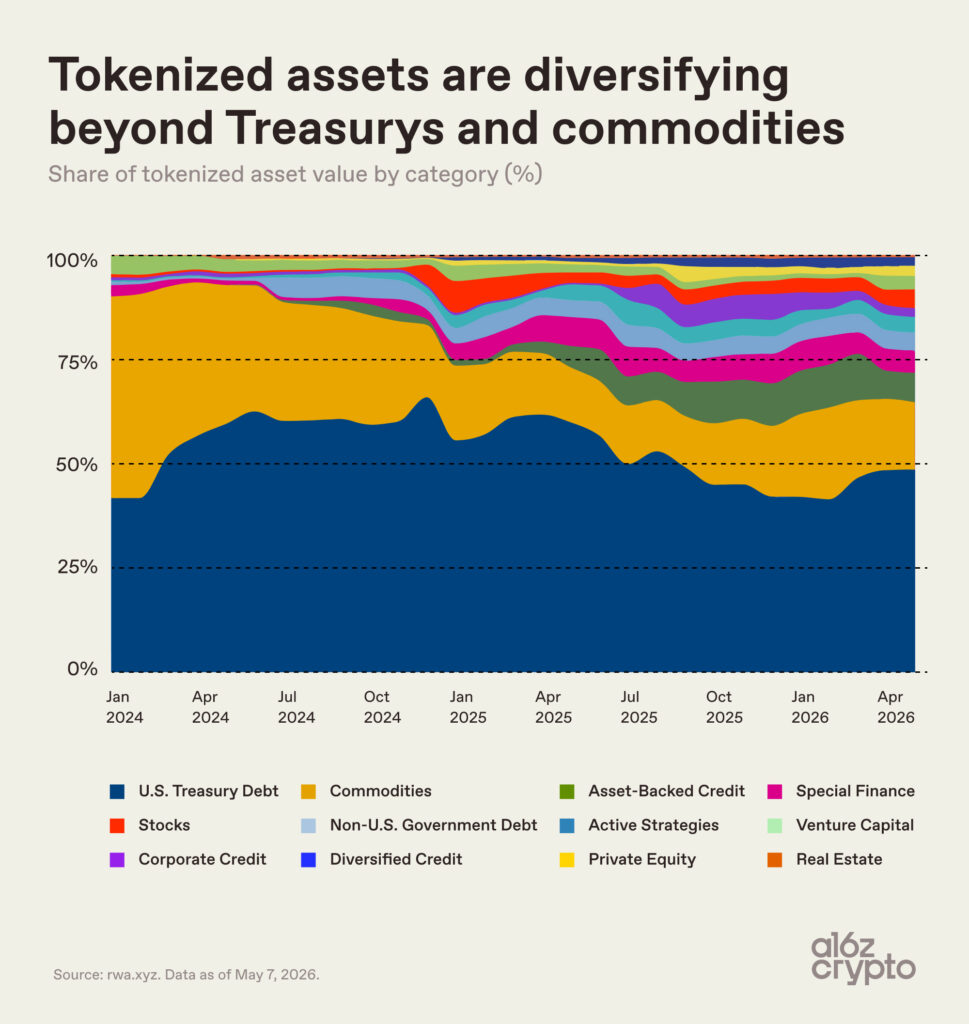

Government debt and commodities scaled relatively quickly — reaching $1 billion in 2–3 years — and since then they have become the most dominant categories. By early 2024, they made up nearly the entire tokenized asset market.

While other categories, like asset-backed credit, specialty finance, stocks, and active strategies, have steadily expanded their share since 2024, the market continues to be highly concentrated. Tokenized U.S. Treasurys and commodities together make up roughly two-thirds of the market today.

A closer look inside the tokenized asset market

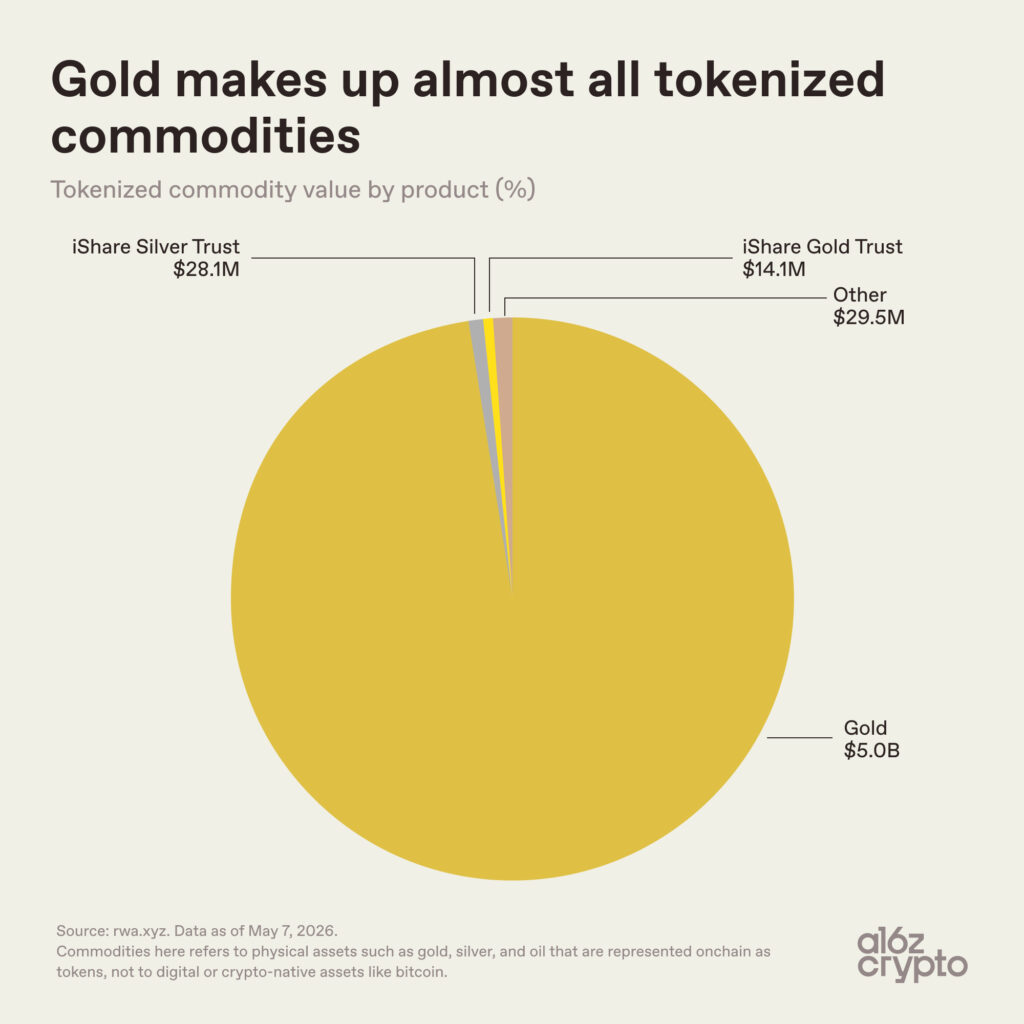

There is even more concentration inside the commodities category: Gold accounts for essentially all of it — roughly $5 billion of a roughly $5.1 billion total. Silver-related and other products barely register in comparison at $57.6 million total, or 0.01%.

Gold is a natural fit for tokenization: It’s globally standardized, easy to store, unperishable, and already commonly traded through paper claims. Crypto investors also have a longstanding affinity for gold; bitcoin was branded “digital gold” long before tokenized gold products existed. Products like Tether’s XAUT and Paxos’s PAXG translate a familiar ownership model onto blockchain infrastructure, turning claims on gold held in vaults into tokens held onchain through wallets.

Tokenized oil, agricultural products, and newer categories — like energy and compute — have exceedingly thin market share and remain more nascent. For now, the tokenized commodity market is almost exclusively a gold market.

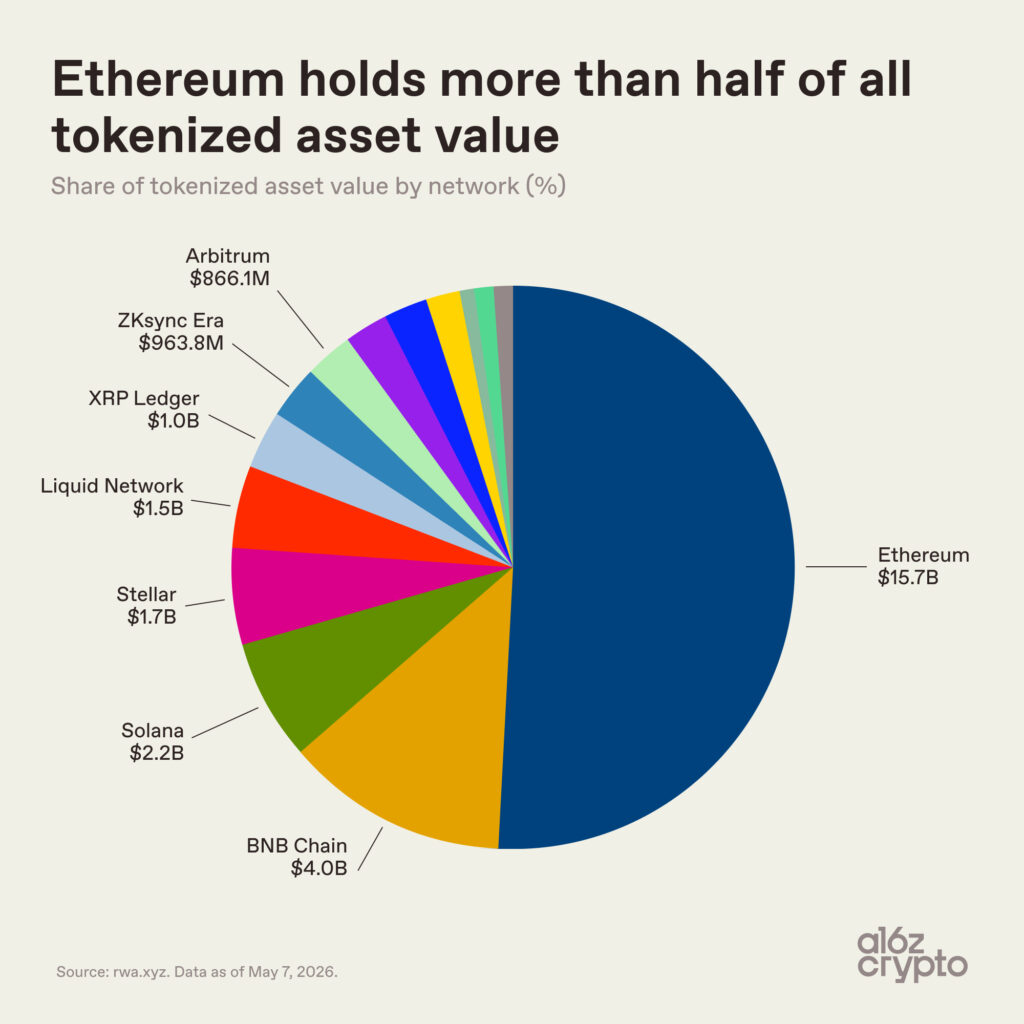

As for the networks that host the tokenized asset market as a whole, the picture is more diversified. Ethereum still dominates tokenized assets, holding slightly more than half of the market at $15.7 billion, consistent with its headstart in DeFi and institutional adoption.

But the rest of the tokenized assets market is multichain: BNB Chain holds $4 billion, Solana $2.2 billion, Stellar $1.7 billion, and Liquid Network (a Bitcoin sidechain) $1.5 billion. XRP Ledger, ZKsync Era, and Arbitrum each approach $1 billion.

Rather than converging around a single chain, tokenized assets are spreading across multiple blockchain ecosystems given criteria like cost, liquidity, compliance requirements, and go-to-market relationships.

The most revealing data point, however, is not in the size of the tokenized asset market…but in how those assets are being used.

Most tokenized assets are not yet ‘composable’

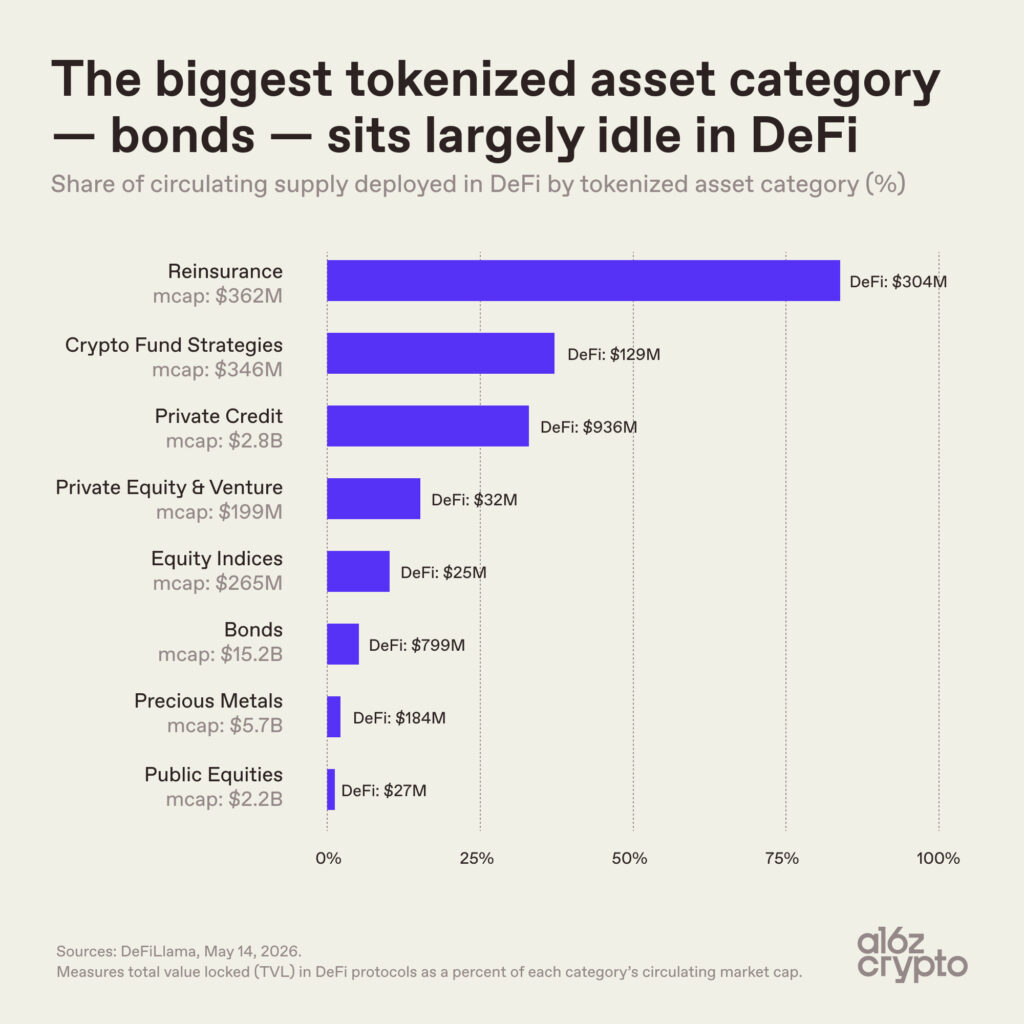

Bonds are by far the largest tokenized asset category at $15.2 billion in market cap. But only about 5% of that supply — roughly $800 million — is deployed inside DeFi protocols.

Precious metals have similarly low utilization rates. These assets are mostly held onchain rather than used as composable financial building blocks that can extend upon, remix, or interoperate with each other.

Smaller categories look different. Reinsurance tokens, with just $362 million in market cap, have 84% of their supply deployed in DeFi, while private credit sits at 33%.

These datapoints make sense: The categories with the highest DeFi utilization rates were built for onchain composability from the start (through protocols like Nexus Mutual and Maple Finance). By contrast, the largest tokenized categories — Treasurys and gold — were designed primarily just to make familiar assets easier to hold and transfer onchain without fundamentally changing how they otherwise behave.

This distinction points to a broader divide within the tokenized asset market itself: Not all tokenized assets are equally onchain.

Some assets are freely transferable and usable across onchain applications. Others use blockchains mainly as recordkeeping infrastructure, with limited transferability or composability. (RWA.xyz, for instance, distinguishes between “distributed” vs. “represented” assets.)

Much of what gets called “tokenization” today is actually closer to digitization: moving records onto blockchains without unlocking composability. This matters because composability is one of the core value propositions of onchain financial systems and could make them much more powerful.

Other attempts to measure “onchain-ness” reach similar conclusions. Pantera Capital’s “token presence index,” which grades tokenized assets on how natively onchain they are, ranks more than three-quarters of assets in the lowest tier. In practice, many of these tokenized assets function as little more than digital receipts representing claims on assets that are still primarily managed through offchain ledgers and intermediaries.

This gap — between assets that are “skeuomorphically” onchain as digital records, and assets that are “natively” onchain in ways that take advantage of the unique properties of blockchain technologies — is one of the clearest signs of how early the market still is.

The infrastructure for composability exists. The assets are there. But the deeper integrations are just beginning.

Where tokenized assets go next

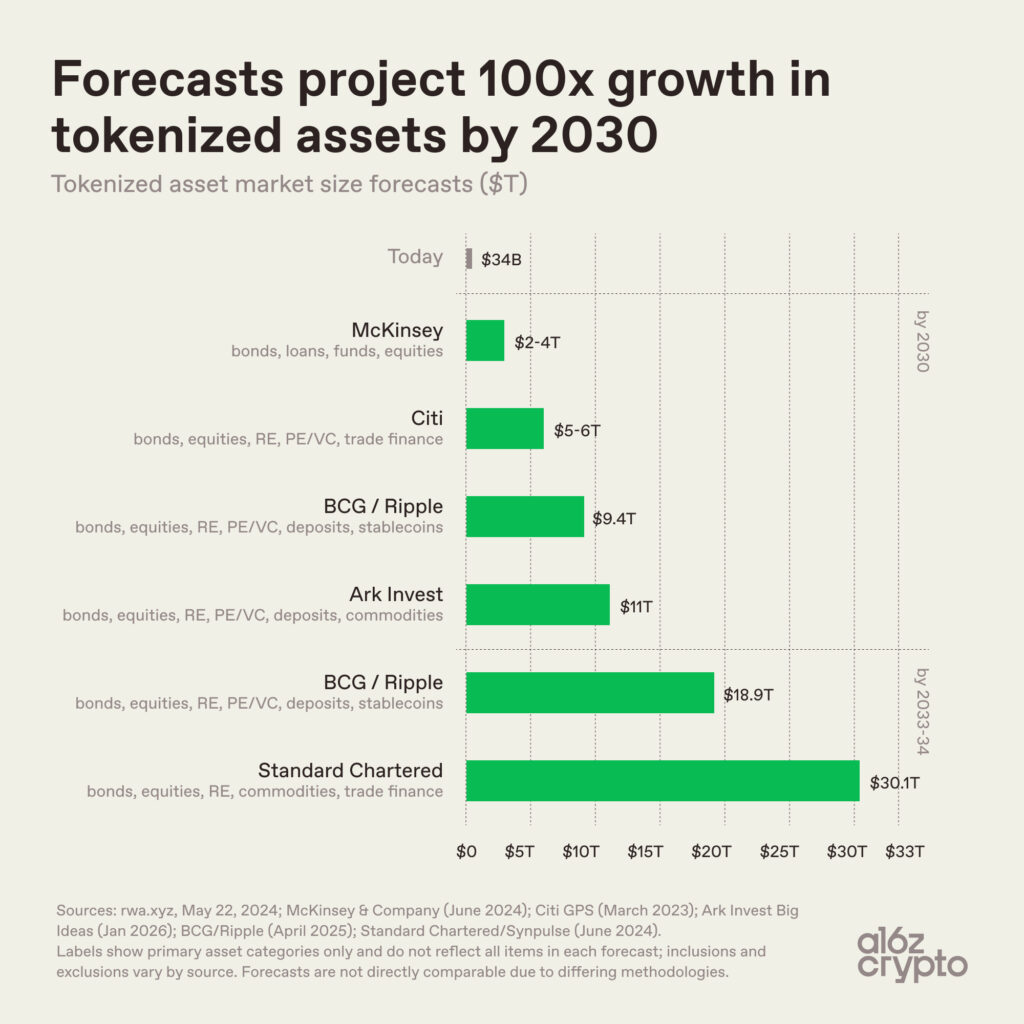

Looking ahead, forecasts for tokenized assets vary in scale, but they are directionally aligned: All point to expansion.

McKinsey’s base case puts the market at $2–$4 trillion by 2030. Ark Invest projects $11 trillion. BCG and Ripple estimate $9.4 trillion by 2030, rising to $18.9 trillion by 2033. Standard Chartered projects more than $30 trillion by 2034.

Every major forecast implies 100x growth from today’s roughly $30 billion market. Where they disagree is on scope.

The gap between $2 trillion and $30 trillion is less a disagreement about adoption rates than about definitions. Different institutions are measuring different things: which asset classes to include, whether stablecoins and deposits count, how broadly tokenization is defined, and so on. McKinsey focuses primarily on bonds, loans, funds, and equities. Standard Chartered adds commodities and trade finance. BCG and Ripple include deposits and stablecoins alongside more traditional asset categories.

Despite those methodological differences, the broader trajectory is consistent across all of them: Asset tokenization is expected to expand far beyond today’s market.

***

Relative to the magnitude of all global finance, the size of today’s tokenized asset market remains a mere blip. The global bond market sits above $140 trillion; tokenized bonds account for roughly $15 billion, or about 0.01%. The total above-ground value of gold is measured in the tens of trillions; tokenized gold, at roughly $5 billion, represents less than 0.02%. Global equities are worth well over $100 trillion; tokenized stocks, at roughly $1.5 billion, remain around 0.001% of the underlying market.

And yet the emerging market is taking shape. The first successful categories were the ones easiest to move onchain: Treasuries, gold, private credit, and other assets with clear pricing, existing demand, and relatively straightforward ownership structures.

In most cases, tokenization has not yet reinvented the underlying assets. It has changed how those assets can move and settle, while only just beginning to connect them more directly to digital financial infrastructure. Much of today’s tokenized asset market remains closer to digitization than true onchain composability. Many assets exist on blockchain infrastructure without yet functioning as programmable financial building blocks.

The harder challenge comes next: bringing more complex parts of the financial system onchain and integrating tokenized assets more deeply into composable, internet-native financial infrastructure.

***

Acknowledgments: Thanks to Ryan Holloway for his helpful input, including proposing the third chart.

***

Robert Hackett is features editor and head of special projects at a16z crypto.

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investment-list/.

The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures/ for additional important information.