DAOs – decentralized autonomous organizations – are an essential tool in achieving the self-empowering benefits of web3, including more equitable ownership among stakeholders, reduced censorship and greater diversity.

DAOs advance web3’s benefits by enabling decentralization. They allow developer companies to hand control of the developed networks and protocols to users, most commonly through the distribution of governance tokens. This process effectively turns the networks and protocols into public utilities that users can then build on top of, knowing that there is no centralized controlling authority that may suddenly change the rules and decide to extract value from them. DAOs are often utilized to control treasuries that incentivize ongoing development of their network and protocols, thereby ensuring that the open source and decentralized technology of web3 will have sufficient resources to continue innovating and improving.

Beyond the network and protocol variety, DAOs come in many flavors. These include:

- Investment DAOs in which individuals, friends, and colleagues form clubs to invest in web3 startups;

- Collector DAOs which acquire NFTs;

- Social DAOs that convene web3 communities;

- Collective/Cooperative DAOs in which groups of artists and engineers deliver services to other DAOs; and

- Charitable DAOs that promote good causes and public goods development.

The variety within these different types of DAOs is demonstrative of communities coming together across the world around shared interests, purposes, and passions.The proliferation of DAOs represents an exciting frontier of the internet’s evolution, but it also spawns many legal, tax, and operations questions. As the number and diversity of activities contained within DAOs grows, so do questions of how these organizations exist as legal entities. We started our Legal Framework for DAOs series last year to assist builders, founders, and members in evaluating their options in an evolving regulatory landscape. We published reference guides – flowcharts and feature comparisons – to help web3 builders a couple weeks ago. In Part II – available for download here – we propose a new pragmatic framework for entity selection and conclude that domestic U.S. entity structures for DAOs provide significant clarity beneficial to the overall growth of the web3.

Evolving the DAO legal entity concept

Formation of DAOs is not an easy process, especially when considering the logistical complications of coordinating a diversified community. This difficulty is compounded by an overall lack of regulatory clarity all over the world. In the United States, little legislative action has been enacted and agencies like the SEC and IRS have not provided critical guidance to web3 builders. That environment has exacerbated the uncertainties involved in selecting a DAO legal entity.In the brief history of DAOs, two entity forms have become the most frequently utilized – and neither comes without risk. The first, Entityless, in some ways represents the ideal form of decentralization, but it limits operational functionality because it lacks legal existence, can’t pay taxes, and potentially exposes participants to unlimited liability (or at minimum, nuisance suits to determine liability). The second, Foreign Foundations, can offer tax advantages by headquartering outside the U.S., but they may, in practice, be highly susceptible to government censorship, thereby severely undercutting their value proposition.

Finding the right fit

Our work has practical, actionable implications for web3 builders today. We argue, for instance, that significant U.S. membership or activity in a DAO limits the long-term viability of Entityless and Foreign Foundation structures. Instead, we propose using domestic entity structures when appropriate, with particular emphasis on the UNA, or unincorporated nonprofit association. The UNA is a compelling alternative that provides legal existence to unincorporated organizational forms, which is analogous to what most DAOs represent. For more detail refer to our initial publication introducing the UNA. The structure is operationally flexible, adheres to the tenets of decentralization (governance by token holders, anonymity, etc.) and despite the name, is not prohibited from earning profits. (Rather, UNAs are limited in how they can distribute profits in a way that’s complementary to current federal securities laws.)

1/ Over the past 6 months, @David_M_Kerr and I have been researching several legal issues facing many DAOs (liability, taxes, contracting, etc.) that are beginning to emerge and that threaten their viability. Today, we published a potential solution.👇https://t.co/eB6XiR1a5R

— miles jennings (@milesjennings) October 26, 2021

In no way are UNAs the right choice for every kind of DAO. Some DAOs might best be established as limited liability corporations (LLCs), limited cooperative associations (LCAs), or other structures. The match depends on the circumstances of a given project. If you’re a builder, a prospective DAO creator, member, or advisor or just an interested web3 participant, you should familiarize yourself with the available options in order to choose an optimal fit – at least until new legislation passes or regulators provide clearer guidance.

To help guide you: Ask yourself the following questions when thinking through which DAO legal entity is right for you.

4 questions to help pick a DAO legal entity

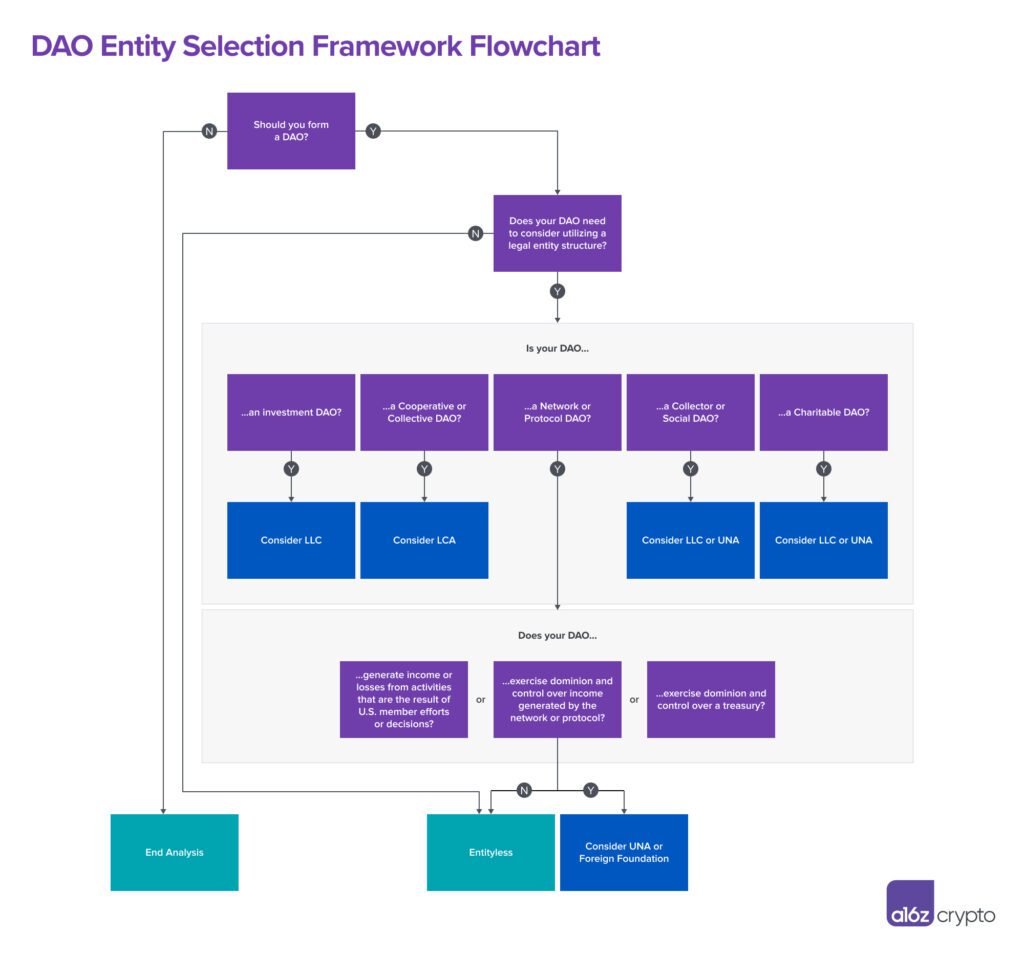

- Should you form a DAO? The question may seem obvious, but it’s worth thinking hard about. Simply slapping a blockchain onto existing business operations to ride a wave of interest in DAOs misses the benefits of building in web3 and creates significant regulatory, liability, and taxation risks. If blockchains and decentralization aren’t essential to your project, you might not benefit from creating a DAO and your organization might best be suited to some other structure.

- Does your DAO need a legal entity structure? Legal entities can have more muscle than their entityless counterparts. Some advantages: Legal entities can, often, more easily manage community-controlled treasuries, own assets and intellectual property, employ people and produce income, and interact with external organizations. In a nutshell, legal entity status provides for a DAO’s legal existence, limits the liability of participants, and helps the organization determine and meet taxation obligations. While there is no perfect legal entity structure available for most DAOs, choosing a suitable existing one can help mitigate risks.

- What type of DAO is it? The purpose of a DAO will often dictate which legal structure is most appropriate, but there is no one-size-fits-all approach. A DAO formed for the purpose of overseeing a blockchain network or smart contract protocol may not be suitable for a different type of DAO. (If you’re involved in a network/protocol DAO, skip ahead to the last question.) An investment DAO might best be positioned as an LLC, like many existing investment clubs. Collector, social, or charitable DAOs could work best as LLCs or UNAs, depending on their particularities. And cooperatives and collective DAOs might consider LCAs, a form that works for many existing co-ops. When determining a DAO’s legal entity, frameworks for existing analogues are a good starting point.

- For network/protocol DAOs: Is there significant U.S. membership or activity and/or does the DAO exercise control over either network/protocol income or a treasury? If the answer is no to all of the above, then you might consider opting for an Entityless structure. But if the answer is yes to any one of these conditions, then the organization’s activities may give rise to U.S. tax obligations for the DAO or its members. We believe U.S. entity structures provide the cleanest path to meeting those obligations.

For the visually oriented, here’s our four-question guide in the form of a decision tree.

download the full DAO Legal Framework Part 2 pdf here

Editor: Robert Hackett @rhhackett

***

Miles Jennings is general counsel at a16z crypto, where he also works with web3 startups & DAOs on decentralized operations, protocol design, and regulatory matters. He was previously a partner at Latham & Watkins.

David Kerr is the principal of Cowrie LLC, which assists clients with risk mitigation strategies on developing web3 issues. He has 10 years of experience in tax strategy, financial accounting, and risk advisory across the tech industry.

***

The views expressed here are those of the individual personnel quoted and are not the views of a16z or its affiliates. This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Please see more here: https://a16z.com/disclosures/.

***

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investments/.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.