Reputation systems present an opportunity for platforms to recognize—and thus incentivize—participants’ high-quality contributions, including content creation, moderation, community building, and gameplay. This is crucial to the growth and sustainability of any web3 project. Yet designing reputation systems requires complex considerations around reputation supply, distribution, credibility, and more. So while many are exploring this space—from DAOs like FWB to play-to-earn games like Axie Infinity and new social platforms like BitClout—builders have yet to agree on the best way to design these reputation systems.

Drawing on our knowledge of economic theory and game design, we argue for a reputation system design based on a pair of tokens—one for signaling reputation and the other for offering liquidity—which could serve as tangible representations of meaningful contributions.

The evolution of reputation systems

The underlying premise behind reputation systems isn’t new. Since the beginning of civilization, we’ve assigned markers of reputation, such as awarding badges for merit or service. In the corporate world, employees are assigned titles or “levels” to indicate their position in the hierarchy—such “tokens” typically determine one’s salary and other benefits.

Gaming has long been a pioneer of digital reputation systems, as well. Players accrue “points” during gameplay that they can convert into in-game “coins” to spend on new skins, weapons, characters, and so forth.

In general, reputation tokens in the crypto world have taken the form of social tokens. These tokens—which can be issued by a variety of entities including people and communities, as well as games and apps—can be used to acquire social capital, access services, and/or translate into rewards (financial or otherwise). Importantly, in the crypto context, social tokens can often represent ownership and uniqueness (in the case of NFTs) and, because they are decentralized and portable due to blockchains, social tokens can be used across the global internet economy, rather than just within the confines of a single platform or decision maker.

The paradox of reputation tokens: Was it earned or bought?

Reputation tokens on digital platforms typically serve two purposes:

- To identify and reward the users who have contributed value to the platform—a form of signaling, which those users can parlay into public reputation.

- To provide a form of compensation that enables contributors to liquefy some of the value they have created into an exchangeable currency.

Yet these two roles are in opposition to each other. A token needs to be exchangeable in order to be liquid. But the more liquid a token is, the less effective it can be as a pure signal of reputation.

To illustrate this point, imagine that reputation tokens are freely transferable. If the tokens were to serve as a trusted signal of reputation quality, then their trading value would be high, making holders willing to trade them. But as soon as the tokens start trading, ownership loses its signaling value, destroying the reputational capital the tokens nominally convey.

For example, a charity could start minting NFTs that it awards to people who’ve completed over 500 hours of community service. But if those recipients can sell their NFTs to whomever they want, then any time you come across a holder, you have to wonder: “Did that person earn their NFT or buy it?” Even if nobody trades their community service NFTs publicly, the possibility of private sale reduces the signaling value. And in a fully liquid market for such tokens, the signaling value washes out completely.

This presents a paradox: if a token can be transferred easily, then those without reputation can simply purchase it, which reduces the token’s ability to serve as a reputation signal.

Remember when it was easy for people to buy followers on Instagram? That made the follower count a much weaker measure of reputation, to the point that brands started looking for engagement metrics that were much harder to “buy.”

That said, high prices can also reduce transferability. For example, CryptoPunks are now so expensive to purchase that nearly all holders must have bought early. This might appear to undo the paradox — restoring the reputation value of the tokens — but since some people are willing to buy CryptoPunks at exorbitant prices to acquire the appearance of reputation, the signaling value may still degrade. There’s also currently a natural boundary on the number of people able to enter the space; imagine this issue at scale when more people embrace crypto.

Moreover, a decline in reputational capital attached to a token can feed back into the market value of the token. If the token loses its ability to signal reputation, then people become less interested in trading it. Indeed, as people started buying Instagram followings in bulk, those followings lost their signaling value, which made them less interesting for influencers to buy. That opened up the markets for buying other forms of reputation, including likes. An “I’m Rich” NFT that nobody believes actually signals wealth isn’t really worth buying.

Making reputation tokens transferable not only reduces their ability to serve as a signal of reputation, it can also diminish their ability to serve as valuable compensation. Thus, establishing reputational capital requires fully (or at least mostly) non-transferable tokens. The question, then, is how to translate reputation into liquidity.

Social capital shouldn’t be bought—but that doesn’t mean it can’t generate liquidity

A token has signaling value when it is conferred by a trusted source, like a brand, university, or government. But in crypto and blockchain contexts, there aren’t necessarily centralized third-party sources conferring that authority.

So a second path to signaling value is to make the token substantially easier to obtain if someone has certain underlying characteristics. For example, high scores in video games are much easier to achieve if you’re really skilled or have worked extremely hard; thus, high scores signal some mixture of skill and effort. High view counts on platforms like YouTube are similarly revealing.

The paradox described above—more easily transferable, less signaling power—arises because making the reputation tokens transferable decouples them from the underlying institutions and/or effort that serve as sources of signaling value.

So what if we instead separate transferability from the token itself? That’s why many games already split scores or points and coins or currency; it’s easy to imagine how spending your “score” could really backfire.We propose a two-token reputation system, whereby one token, which we call “points,” serves as a non-transferable reputation signal. A second token, “coin,” is a transferable asset dispensed to holders of points on a regular cycle. Effectively, points spin off dividends in coins that can be used as tradable currency. Moreover, because coins accrue to holders of points, coins also have a link to the underlying reputation.

At a high level, this design promotes a feedback loop whereby users derive points from high-quality contributions on the platform such as contributing content, moderating, or winning gameplay. And then, when the users with points receive coins, they can be traded as a currency. Users’ demand for coins drives the need to acquire points, which in turn incentivizes high-quality contributions.

Note that while we use the language of points as non-fungible and coins as fungible, the precise implementation can vary across applications. The key is that contributors receive a non-tradable token that spins off tradable tokens.

Points should reward contributions

In order for points to maintain signaling value and incentivize high-quality participation, they must be somehow linked to users’ contributions. In the context of a game, points might simply be awarded algorithmically, as a function of performance. On creator platforms like YouTube or TikTok, points could be a direct function of people’s engagement with a given creator’s content. In other contexts, such as publishing platforms like Mirror, there may be a set of users endowed with the ability to reward points, or a governance/voting process that determines point allocations.

What’s important is that points must credibly link their holders to the source (or driver) of reputation. Additionally, the rate of awarding points as a function of contributions would need to be well understood, so users can have a sense of how much effort they need to put in to achieve a given point level. Put differently: participants need to know the rules of the game before they start playing.

In many cases, points don’t need to be scarce. For example, there is no cap on the number of badges that Discord can give moderators. However, scarcity can raise or reinforce the reputation value of the system. For example, the “moderator” role on a Discord server is only given to a select few, so someone who has a moderator badge is seen as having a higher reputation on the server. And if the server started making too many people moderators at once, the perceived meaning and value of the role would degrade.

Size matters: The importance of dividends, supply, and distribution

To create a form of liquid value attached to reputation, coins should accrue to point holders through a series of dividends, where each point holder is awarded coins based on the number of points they have.

There are three key questions in the design of such a system:

Size: How big should dividends be?

The total size of each dividend—that is, how much coin is distributed each time a dividend is issued—depends on the macroeconomic goals of the system.

Unlike with points, it is important that coins be relatively scarce in order to give them value as a currency. Many currencies (such as Bitcoin) benefit from a long-run limit on coin supply — there’s only so many of them that can ever be minted. In such cases, the average total dividend must be decreasing over time, unless there is some mechanism by which coin is absorbed back into the system (such as through within-platform payments).

Even so—and contrary to some standard intuitions—coin supply does not necessarily have to be bounded. If, for example, coins are redeemable for a share of a platform’s treasury, then the total coin supply can expand as the treasury grows. In these cases, dividends could be the same total size, or even growing over time, so long as the dividends are spaced apart enough that they don’t outpace the treasury’s growth.

Supply: How frequently should dividends be issued?

For platforms where participation functions like employment, as with gig or creator platforms, the optimal strategy would be to distribute coins to point holders at a regular interval: for example monthly, or even daily. That means the users who make valuable contributions, thus maintaining a certain point level, receive a stable income.

Infrequently or irregularly scheduled dividends are more appropriate for platforms where contributions aren’t as regular, as in some DAOs. For example, Forefront issues its $FF token when a member contributes an article or works on a coding project. An alternative is for coins to be issued only when platform engagement, productivity, or funding exceeds a threshold. This is similar to public company dividends, and we also saw it in the case of Mirror’s $WRITE token airdrop.

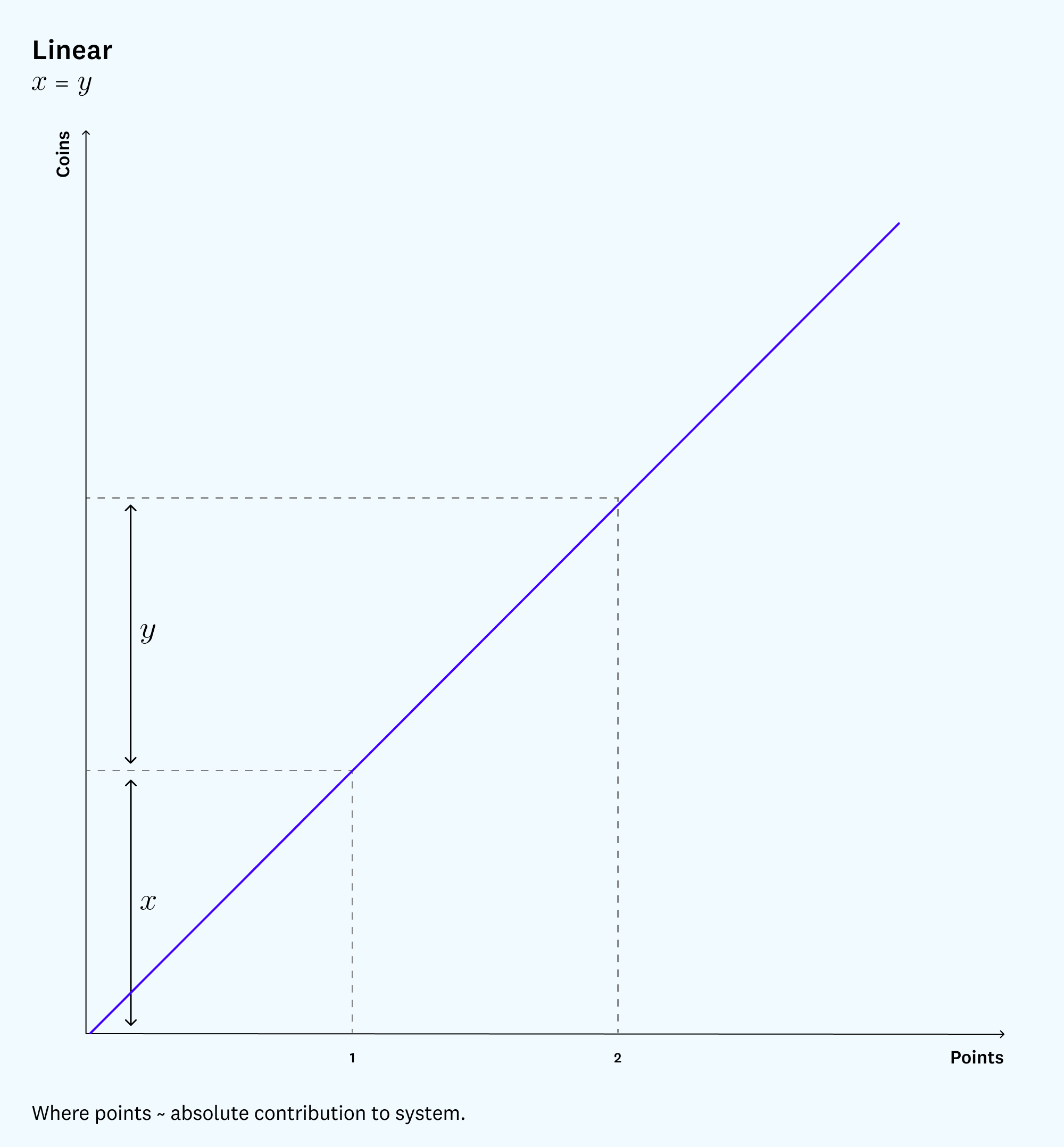

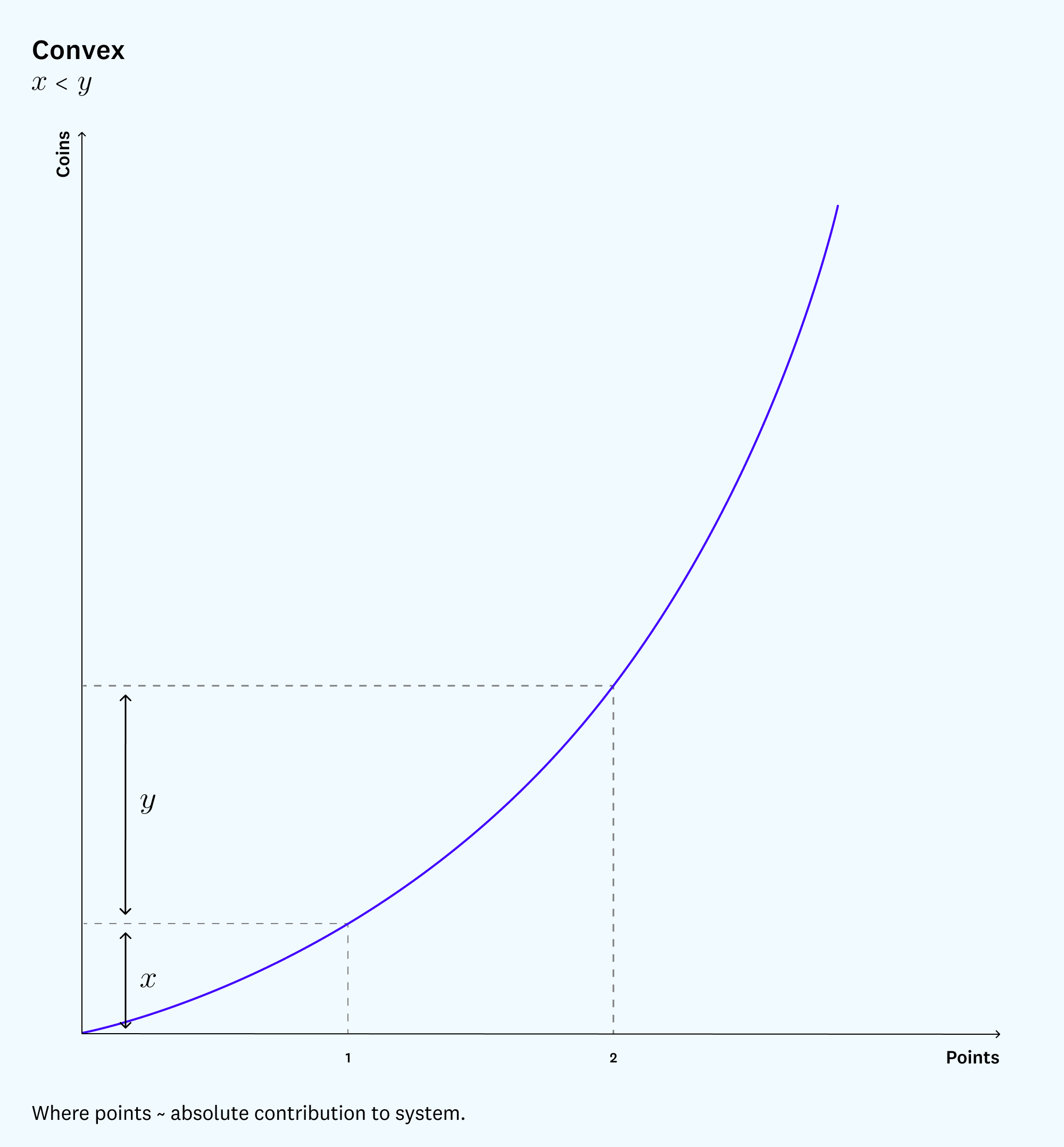

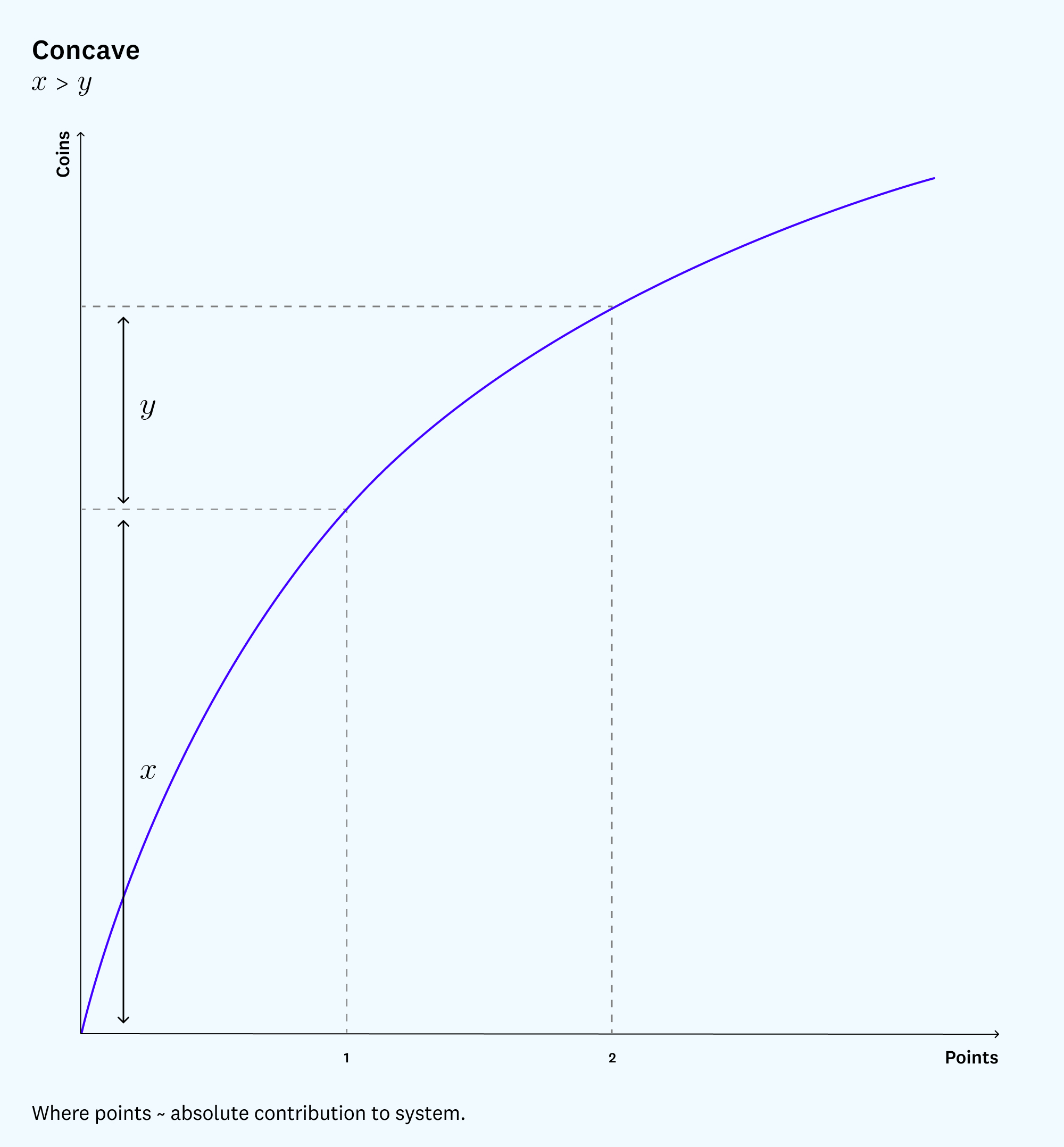

Distribution: How should the size of the dividends relate to point holdings?

Perhaps the easiest way to link coins to points is through linear dividends, whereby each point entitles a user to an equal share of each dividend. But this isn’t the only option.

Under a convex dividend rate, a disproportionately larger share of each dividend accrues to users with larger numbers of points. That is, the increase in dividend in going from 1 point to 2 points is higher than the increase in going from 0 to 1. A convex rate rewards users who have been engaged in the system for a long time, providing more incentive to maintain status.

The opposite approach is a concave dividend rate, in which going from 0 points to 1 is worth more than going from 1 to 2. This approach is ideal for drawing new users in, as it rewards initial contributions more than later contributions, whether your second, third, or 27th. That said, a concave rate system like this is harder to maintain if users are anonymous, since in that case users can create many accounts and earn “early” points with each of them.

Financial rewards should align with contributions

The three dividend design features—size, supply, and distribution—determine the number of coins a point holder receives in each time period. This relationship directly impacts the incentives to acquire points.

Ideally, the distribution of coins should be calibrated so that a user’s marginal return for acquiring points corresponds to the marginal benefit of the point-generating activity to the platform. How you think about this marginal benefit depends on the way in which contributions create platform value. In other words, you should earn points based on how much value you’re creating for the platform.

On platforms like YouTube, for instance, points would reflect video views—and the platform can precisely estimate how much a given view contributes to platform engagement and the bottom line. The platform should then issue coins to each creator in proportion to the marginal value of their views. Here, convex dividends may make sense, since “top” YouTubers drive more long-term engagement than less popular ones. YouTube went through a few iterations of this—initially tying payout to views, then to watch time and, most recently, to an engagement metric they’ve named “YouTube time” that considers more than just time spent watching content on the platform.

YouTube constantly tweaks how much it pays out. This creates income uncertainty for YouTube creators who are paying bills from their ad revenue payouts. Ideally, a platform would make how much participants earn for their contributions more transparent, so that contributors can assess the value of acquiring points (as well as avoid frustration and burnout).

Additionally, the principle of marginal return = marginal benefit implies that the rules for point allocation might have to be adjusted. That enables the platform to give a disproportionate share to early contributors, commensurate with the importance of their contributions to the system when it was less proven. That said, the platform may not have a clear sense of the contributions’ value, especially early on, so there needs to be a mechanism for experimentation and recalibration around token distribution.

Reputation incentives must be ongoing

The link between points and coins provides a natural mechanism to reward users who have made high-quality contributions. But because points are non-transferable, there is an element of hysteresis: those who accumulate points early could end up owning a disproportionate share of the dividends, especially if the asymptotic coin supply is fixed.

In many crypto projects, the largest holders end up being just the people who were aware of the project earliest. But those early adopters are not necessarily the most valuable to the future of the ecosystem. So it is essential to maintain incentives for ongoing contributions and engagement. One natural way to achieve this in a two-token framework is to have points degrade or depreciate over time. This can be implemented by decreasing dividends as a function of the age of user points. But an even easier implementation is to simply have a user’s point totals decline, either mechanically over time or as a function of the user’s engagement level relative to others.

This is again analogous to what happens in gaming: With absolute leaderboards, points are zero-sum—if a player does not maintain their contributions, then they eventually lose their standing as other players overtake them. The same is often true on creator platforms, where competition for consumer attention incentivizes ongoing participation.

But even when the point pool itself is growing, rather than zero-sum, there may be value in having points degrade mechanically simply to create participation incentives. There also may be value in explicitly specifying the rate and causes of point degradation, as it could help users optimize their contributions levels.

Point degradation means that coin dividends are like a stock dividend with automatic dilution over time, in the same way that traditional public firms dilute their equity by issuing new shares precisely when they need new investment to grow their value. In this sense, point degradation reflects the need for continuing user investment in the platform.

And of course, as with any currency system, the actual value of coins depends on the community’s perception of that value. This implies that the value of points depends in large part on the perceived value of coins. Thus, the community’s perception of a coin’s value needs to be at least high enough to back the total coin in distribution.

This means the platform may need to undertake monetary policy—tweaking total money supply, perhaps through buybacks or temporary trading restrictions. For example, in the first few weeks after launch, BitClout didn’t allow the exchange of BitClout to other currencies. The two-token system we have described offers a simple alternative approach: adjust either the point accrual rate or the dividend flow rate. For example, the council that governs a game could make the game slightly harder, as a way of slowing down point accumulation, or could reduce total dividend size, as a way of decreasing the long-run coin supply.

But builders have to be careful with these sorts of interventions, as every change in the overarching incentive structure for contributors impacts contributor behavior. In particular, anything that degrades point value unexpectedly could harm user trust.

Don’t overfinancialize it

We’ve outlined some core principles of social token design, but it’s equally important to complement such designs with product-market fit that intrinsically motivates users. For example, a play-to-earn game that focuses its efforts on enabling users to profit but that doesn’t get the “play” element right misses the point: that games are, first and foremost, supposed to be played for fun.

A product that’s bootstrapped around a reputation system but lacks true product-market fit risks creating a community of speculators, rather than of actual users.

But once product-market fit is achieved, incentive dynamics take over. It would be very difficult for a platform to scale and reach mass adoption if it doesn’t reward users properly. To make the incentives work, a reputation system should separate social capital from financial capital, particularly if the former offers a clear path to the latter.

* * *

There’s much more to consider here, such as the relationship between governance and reputation; making the reputation system responsive to the evolution of the contributor community; and making reputation building accessible for all types of contributors. But we believe that if builders embrace the two-token system design at a high level, they’ll be able to reward contributors with an authentic reputation signal that holds its value even while generating liquidity. That’s precisely what these projects need to drive growth.

Acknowledgments: This essay is a response to a community request via GhostKnowledge. Thanks to Sari Azout, Christian Catalini, Far, Jihad from Forefront DAO, and David Phelps for their input.

Disclosures: Jad Esber is an investor in a number of NFT and DAO projects. Scott Kominers provides market design advice to a number of marketplace businesses and crypto projects, including Novi Financial, Inc., the Diem Association, and Quora.

***

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investments/.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.