There’s a lot of talk lately about the possibility of a prolonged financial downturn, reminiscent of 2008. 2008 was a difficult time for many people.

But from a startup perspective, 2008 and the following 3 years turned out to be a golden age. Apple released the iPhone in 2007 and the app store in 2008. By 2009 talented founders were pouring in.

Most of today’s top mobile apps were created by companies founded between 2009 and 2011, including Uber, Venmo, Snap, and Instagram.

In retrospect, that era was propelled by a combination of three powerful trends: social media, cloud computing, and the rise of smartphones.

Independent product design spaces are multiplicative: even if social, cloud, and mobile each improved linearly, the combination could improve exponentially.

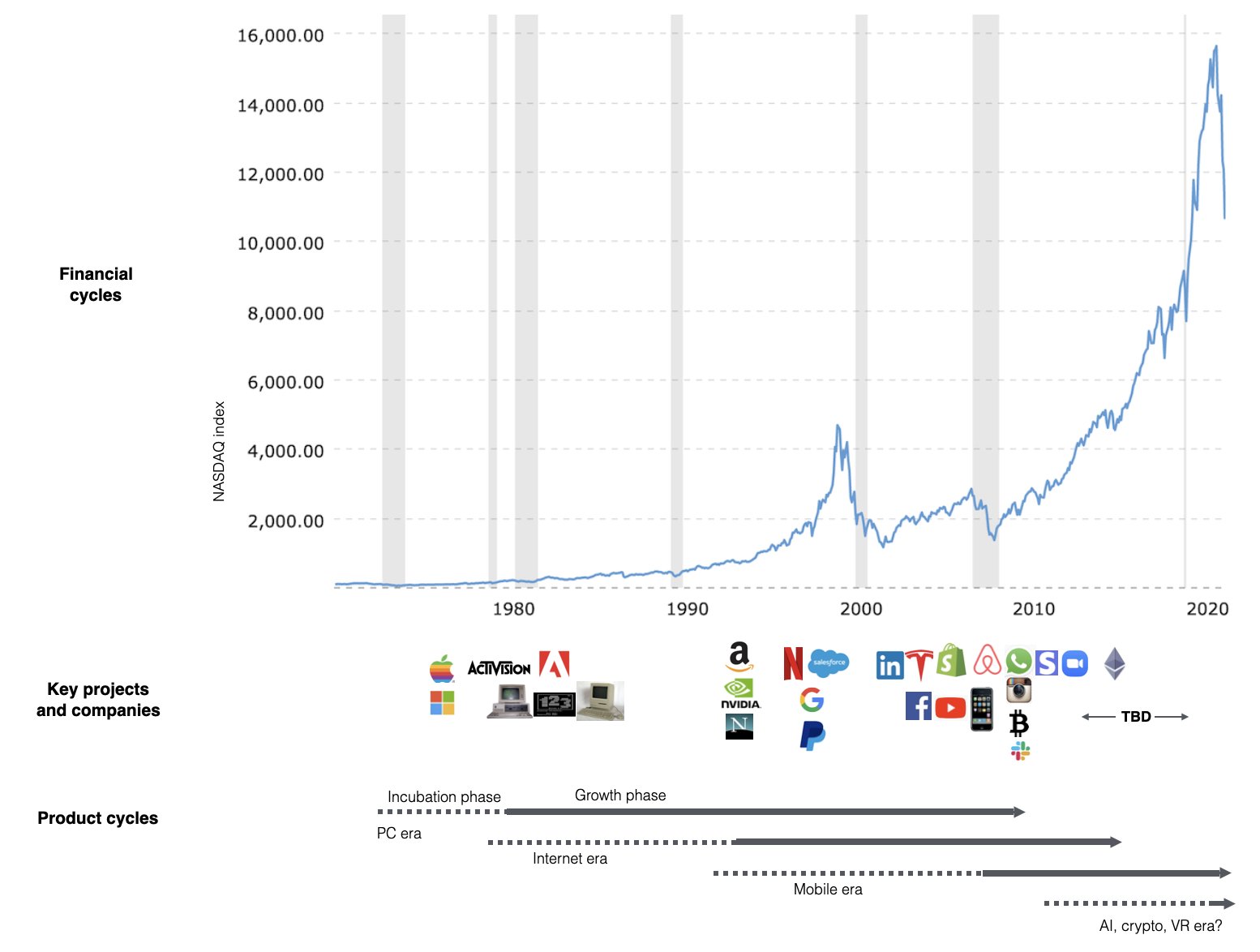

I made the chart below to summarize how I’ve come to think about product and financial cycles.

The key idea is that product and financial cycles evolve mostly independently. The top of the chart shows the Nasdaq index as a rough proxy for financial sentiment. Financial sentiment fluctuates unpredictably and sometimes wildly.

The next row shows the years that iconic startups or products were created. The timing is mostly dictated by product cycles, which are shown in the bottom row.

Product cycles follow their own internal logic and tend to be more predictable than financial cycles.They begin with an incubation phase in which enthusiasts explore ideas and build products that are mostly used by other enthusiasts.

For example, there were credible attempts to create smartphones as early as 1990. Smartphones continued to advance for the next 15 years, but it wasn’t until after the iPhone launched that they transitioned from the incubation to the growth phase.

The growth phase starts when the right mix of technology, talent, and community knowledge comes together. It is driven by a reinforcing feedback loop between infrastructure and applications.

For example, as the iPhone improved, better apps were possible. Better apps helped drive iPhone sales, giving Apple more money to invest, enabling even better apps, and so on.

The tech industry is very different today than it was in 2008. A handful of tech incumbents dominate the internet, exerting vast economic and cultural influence. Entrenched interests aggressively respond to new movements that might someday threaten them.

I believe crypto and web3 will be at the center of the next cycle. We’ve reach a critical mass of technology, talent, and community knowledge. In the almost 10 years I’ve been involved in the space, the energy and creativity has never been higher.

If we are headed for an economic downturn, there are some tactical lessons from the 2008 era, namely preserving capital and staying focused on your long-term vision. But the main lesson is to ignore the noise and stay squarely focused on the product cycle.

***

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investments/.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.