The DUNA: An Oasis For DAOs

Everyone active in web3 has heard the term “DAO”, short for decentralized autonomous organization. DAOs are a critical tool for keeping blockchain networks open, but they’ve also struggled to achieve success in web3 and have become a target of legal and regulatory actions.

This week, Wyoming passed a new law to recognize DAOs as legal entities, enabling blockchain networks to operate within the bounds of applicable laws without compromising their decentralization. This is a major breakthrough as it will provide DAOs with much-needed protections and empower them to keep blockchain networks open.

Wyoming has a long history of supporting innovative legal entity structures. The state was the first to adopt the limited liability company (LLC), the first to adopt the unincorporated nonprofit association (UNA), and the first to introduce a subset of its LLC statute to be utilized by DAOs. The new Wyoming law incorporates many of the provisions we proposed in the model legislation published here.

This new entity structure is likely to become the industry standard for blockchain networks created in the United States. So, here’s everything you need to know about Wyoming’s Decentralized Unincorporated Nonprofit Association (DUNA).

1. WHAT IS A DUNA?

On March 7, 2024, SF50, the Wyoming Decentralized Unincorporated Nonprofit Association Act, was signed into law with an effective date of July 1, 2024. The bill was closely modeled on Wyoming’s existing Unincorporated Nonprofit Association Act, but it is purpose built for decentralized organizations.

Just as Wyoming’s previous DAO law (W.S. 17-31 Decentralized Autonomous Organization Supplement) can be thought of as a “Digital LLC”, SF 50 can be thought of as a “Digital UNA.”

Additionally, people can think of it as the Web3 equivalent to a town council. The council’s purpose is to protect the township’s standards and operations by enforcing the codes and covenants of the community, which ultimately serves the interests of its citizens, their homes and their businesses.

Similarly, the purpose of a DUNA is to protect and support the underlying blockchain network, but like a town council, it is not itself a business.

2. WHY IS IT NECESSARY?

Entrepreneurs around the world are using blockchain technology to build a better internet – one that returns the Internet to its foundation as an open network. But, if we leave it to corporations to own these networks, we’ll end up in the same place we are now, where our entire digital world is intermediated and controlled by a handful of monolithic companies.

Blockchain technology offers a compelling solution to this problem. It enables the creation of open blockchain networks that function more like public infrastructure than proprietary technology – anyone can build on them, just like anyone can currently build a business using open internet networks like email and websites.

DAOs are made up of members of a community that governs the affairs of an open blockchain network. They are a critical tool for ensuring that the network remains open, that it does not discriminate and that it does not unfairly extract value. The DUNA helps DAOs accomplish this by solving three of the key challenges they face – it gives them legal existence, enabling them to contract with third parties and appear in court, it enables them to pay taxes and it provides them with limited liability from the actions of other members. All of these are commensurate with other legal entity forms and are table stakes for building in America.

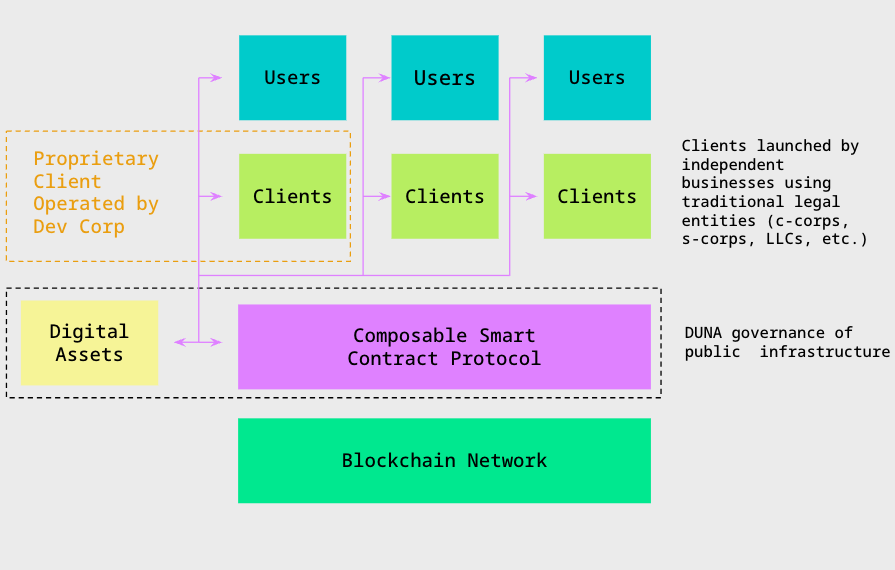

The DUNA solves these challenges without exposing consumers to additional risks. A DUNA can be used for the decentralized governance of open blockchain networks, but anyone building a consumer-facing application like a social media app, car service, or music streaming app on top of these open networks would continue to use traditional entity forms, like the corporation or LLC. And even though this paradigm includes the use of corporations, the fundamental difference is that corporations no longer control the underlying networks, they only control user-facing apps. That difference greatly reduces their ability to extract value like web2 companies do.

The Future of web3: Proprietary clients operating as ordinary internet businesses, but built on top of public infrastructure comprised of smart contract protocols and blockchain networks that are run by DAOs.

3. WHY SHOULD DAOs USE THE DUNA?

DAO membership and participation is currently fraught with peril. DAOs that fail to use a legal entity for their organization are deprived of legal existence, are unable to pay taxes and are exposed to potential liability. A lack of legal entity also threatens the privacy of DAO members. As a result of these risks, the failure to use a legal entity has impeded the decentralization of blockchain networks, limited their growth and stunted the development of economic models for such systems.

If DAOs fail to adopt legal entities, this problem is likely to get worse before it gets better. Regulatory actions and class action lawsuits in the United States have alleged that without a legal entity, a DAO is just a general partnership. While there are several viable arguments that challenge these allegations, that categorization would be catastrophic for DAO members, subjecting them to untenable tax risk and legal liability. Momentum is currently on the side of the regulators and plaintiffs firms. If their theory propagates and succeeds, it will likely be a death knell for decentralized governance.

The DUNA stops this vector of attack dead in its tracks, solving the key challenges DAOs face and substantially mitigating the risks facing DAO members. It provides DAOs with legal existence, enabling them to contract with third parties, open bank accounts and provide an easy vehicle for the service of process. It enables DAOs to pay taxes and meet their informational reporting requirements. It protects DAO member privacy from the federal government. And it provides DAO members with liability protections.

It accomplishes all of this without interfering with how DAOs are currently launched and operated – it safeguards decentralization and positions DAOs to effectively grow the ecosystems of their underlying blockchain networks.

4. IF DUNAs ARE NONPROFITS, CAN THEY ENGAGE IN FOR PROFIT ACTIVITY?

Yes. Under Wyoming law, both the UNA and the DUNA are able to engage in for-profit activities. This would include the operation of a decentralized exchange protocol, a decentralized social media protocol, you name it.

Wyoming’s DUNA statute also specifically permits the payment of reasonable compensation for any services provided to a DUNA’s ecosystem. This feature is expected to enable DUNAs to compensate the members that help foster their growth without needing to extract value from users. That’s critical as it ensures that blockchain networks can operate in a decentralized manner and compete with centralized corporate networks.

Using this feature, a DAO could, for example, pay compensation to its members in exchange for participation in governance. In that case, the justification for the DUNA rewarding people for voting or delegating might be that by statute the DUNA doesn’t have centralized management and is therefore reliant on its members to govern all of its affairs. As a result, significant participation is necessary in order to ensure proper administration of the DUNA, and the DUNA can compensate members to achieve that end.

While Wyoming courts will ultimately determine what compensation is reasonable, there are ample real world examples of nonprofit organizations to draw inferences from. In addition, the unique characteristics of blockchain networks provide a strong foundation for arguments about the reasonableness of robust member compensation. For example, because blockchain networks are typically open source and can be “forked” (duplicated) by anyone, the continued prominence and use of a particular blockchain network that collects fees and distributes compensation to members, is an implicit endorsement by users of such network that the compensation it is paying is reasonable. If it weren’t, an alternative network would be launched.

Nevertheless, the “reasonable” qualifier does present a ceiling on the value that a blockchain network can extract from users and compensate members with. While those that wish to design vertically integrated and centralized blockchain products and services may balk at hurdles to value extraction, this notion is consistent with the spirit of blockchain networks, not antithetical to it. Web3 will be a failure if web3 blockchain networks are ultimately built to extract value from users in the same manner that web2 corporate networks currently do (e.g., Apple’s 30% takerate on AppStore products). Wyoming’s approach supports the web3 ethos, while still enabling cash flows to digital asset holders. This is a significant breakthrough.

5. WHAT ARE THE INITIAL SECURITIES LAWS IMPLICATIONS OF USING THE DUNA?

Under the Howey test, which is the test that determines whether U.S. securities laws should apply to a digital assets transaction, three elements must be satisfied. There must be (1) an investment of money, (2) in a common enterprise, (3) with a reasonable expectation of profit primarily based upon the managerial efforts of others.

Proponents of blockchain technology have long argued that none of these prongs is satisfied with respect to the vast majority of digital asset transactions. Most of these arguments would be maintained or could even be strengthened by a DAO adopting a DUNA legal entity form.

For example, use of a DUNA substantially strengthens arguments that the third prong of Howey is not satisfied with respect to transactions in the digital asset of that DUNA. First, the DUNA is an inherently decentralized entity form whose baseline structure does not include a management function. There are no officers and directors. Second, DUNA members have no statutory obligations or rights with respect to the maximization of the organization’s profits. Together, these features substantially discredit any claim that a member, in acquiring a digital asset, could have had a “reasonable expectation of profit primarily based upon the managerial efforts of others.” Finally, as discussed above, the nonprofit characterization limits the ability of a DUNA to distribute the profits of the organization to its members, but does permit it to compensate members for their contributions to the organization. As a result, any members receiving compensation would, by necessity, not be profiting off the managerial efforts of others, but would instead be profiting from their own efforts.

Nevertheless, it is possible that the SEC could seek to argue that the DUNA satisfies the “common enterprise” prong of Howey because membership in the DUNA is denominated in the digital assets of the DAO. However, there are many counterarguments that can be made based on the decentralized structure of the DUNA. Furthermore, regulators have already sought to designate DAOs as either general partnerships or unincorporated associations under common law, which are no more or less appropriate for establishing “common enterprise” as the DUNA. Finally, the rights of DUNA members are largely a product of the DUNA’s governing principles, which will typically be the rights set forth in the underlying governance and protocol smart contracts that formed the DAO, which would be present regardless of whether or not the DAO formally adopted the DUNA structure. As a result, if the underlying governance smart contracts are not sufficient to establish a “common enterprise”, it would not be reasonable to argue that the presence of a DUNA changes that conclusion.

While SEC theories about the applicability of U.S. securities laws to digital asset transactions are amorphous and constantly changing, the fact remains that they are bound by the Howey case law and its progeny. Under that case law, adoption of a DUNA can be used by a DAO to bolster its community’s arguments against the application of securities laws to the digital assets of that DAO.

6. WHAT ARE THE TAX IMPLICATIONS OF USING THE DUNA?

As will come as no surprise to anyone who has consulted with a tax advisor about DAO taxation, a project’s individual facts and circumstances are the most critical in formulating answers to specific questions and generalities are not a substitute for project specific advice.

Like the LLC and the UNA, the DUNA can remove complexity as to how DAOs will be treated under United States tax laws because of their ability to be taxed as corporations. Corporate tax treatment allows for UNAs and DUNAs to pay their tax obligations in a manner that would not require the disclosure of individual members and avoids the complexity of pass-through taxation, resolving an issue which would be universally problematic for blockchain network DAOs. Additionally, the United States has a significant number of tax treaties with countries where DAOs are likely to have members and provides an environment where utilization of a domestic entity provides significant clarity in tax obligation.

To be clear, the totality of the above does mean that DAOs would have tax payment obligations resulting from their activities that may differ from what currently exist, but ultimately these payments would significantly decrease the risk associated with membership and provide clarity in an uncertain tax environment. By paying tax somewhere and having that somewhere by the United States – DAOs are able to resolve a huge question mark around their operations and membership risk.

7. WHY HAVEN’T MORE DAOs ADOPTED THE UNA ENTITY FORM?

As the DUNA structure was only recently introduced, there have not been any thorough critiques of the structure. However, several arguments have been made against use of the UNA, the statutory predecessor to the DUNA. Those arguments and their respective counterarguments in light of the passage of Wyoming’s DUNA are summarized below.

In short, the arguments against use of the UNA have either been addressed by the DUNA or are not compelling. While it is true that DAOs will continue to be exposed to uncertainty despite adoption of a DUNA structure, it is indisputable that the uncertainty surrounding DAOs will be greatly reduced. While there are some who may wish for a perfect legal entity structure to arrive that affords DAOs and blockchain technology special treatment under the law, this is an impractical approach that forestalls real progress.

- Nonprofit Status Limits Flexibility – Some have argued that the UNA is not an appropriate structure for DAOs due to its nonprofit characterization. This is a fundamental misunderstanding of the “nonprofit” designation. By statute, both the UNA and the DUNA are able to engage in for-profit activities. Furthermore, they permit paying compensation to members. Wyoming’s DUNA statute explicitly permits the payment of reasonable compensation (including in exchange for participation in governance of the DUNA).

- Undermines Decentralization – Some have argued that the UNA introduces centralization risk. While UNAs often require reliance on “managers” to manage the day-to-day affairs of the UNA, DAOs could have easily constrained such powers. In any event, any concerns regarding centralization have been addressed by the DUNA, which is specifically designed for large, decentralized organizations. It works for 100 members just as well as it works for 10 million members. Further, the DUNA contemplates a baseline structure that does not include a management function, but instead allows for the selection of administrators with limited authorization to perform specific tasks authorized by the membership. Such type of activity is already undertaken for most DAOs by protocol foundations, so does not present any greater risk of centralization. This categorization therefore aligns the DUNA with applicable standards for decentralization under U.S. securities laws.

- Jurisdiction Selection – Some have argued that DAOs are not located in any jurisdiction and should therefore not elect to adopt an entity in any jurisdiction, including the UNA. There are many problems with this argument, but put simply, it is fantastical — it fails to contemplate the consequences of what it proposes. Failing to avail oneself of the laws of any single jurisdiction means that one may be subjected to the laws of all jurisdictions. As a result, this approach favors would-be-attackers (both individual plaintiffs as well as governments) by enabling them to bring suit in the jurisdiction that is most favorable to them. This is not theoretical. It has already begun to play out in a regulatory action brought against Ooki DAO and in class action lawsuits brought against Compound DAO, Lido DAO and others. These actions are predominantly being brought in California under the theory that such DAOs are general partnerships. The Ooki DAO court already determined that the Ooki DAO was a general partnership, and if that decision is broadly replicated, it will be a death knell for decentralized governance in web3. DAOs ignore this risk at their own peril.

- Undermines Permissionlessness – Some have argued that use of a legal entity undermines the permissionlessness of DAOs, as it requires DAO members to join the legal entity. Under the DUNA, this is not correct. Holders of a digital asset of a DAO do not need to join its DUNA and may freely elect not to do so. Ultimately, it is up to the DAO to dictate the terms of membership in the DUNA in accordance with the DAO’s governing principles.

- Unclear Use Case/Untested in Courts – Some have argued that because existing UNA legislation did not contemplate use by blockchain networks, state legislatures may not have intended for such structure to be used by blockchain networks, and that the use of UNAs by blockchain networks has not been tested in the courts. These arguments are no longer relevant as the DUNA was specifically designed for decentralized organizations and contemplates use by blockchain networks. Further, use of entityless structures by DAOs have already resulted in courts applying general partnership law, which should strongly dissuade DAOs from remaining entityless.

8. HOW DOES A16Z CRYPTO PLAN TO SUPPORT USE OF THE DUNA?

a16z crypto intends to facilitate the widespread use of the DUNA across web3 so that it becomes an industry standard. These efforts will include (1) creating decentralized governance proposals for adoption of the DUNA for DAOs that it is currently a member of, (2) assisting its existing portfolio companies with the adoption of DUNA structures in connection with their pursuit of decentralization and (3) where appropriate, requiring, as a condition of investment, that its prospective portfolio companies in the United States agree to adopt the DUNA structure upon their decentralization and adoption of decentralized governance. Further, a16z crypto intends to expend considerable effort producing resources for entrepreneurs, law firms, accounting firms and other advisors to facilitate adoption of DUNA structures.

Adopting a DUNA entity structure resolves much of the uncertainty that DAO members currently face when engaging in DAO activities. As a result, we expect adoption to empower DAO members to contribute more and bolster decentralization. For a16z crypto, this means unlocking the full potential of its engineering and research teams to advance the interests of DAOs.

9. WHERE CAN I LEARN MORE?

For background and more information on DAOs, UNAs and DUNAs, see:

- Legal Framework for DAOs (Oct 2021) – Provides background on DAOs, explores the challenges they face, introduces the UNA as a compelling option for DAO structuring and recants the history of the structure.

- Legal Framework for DAOs – Pt II – Entity Selection Framework (June 2022) – Provides a comprehensive argument for why the UNA is the only suitable entity structure for blockchain network DAOs.

- Legal Framework for DAOs – Pt III – Model Decentralized Unincorporated Nonprofit Association Act (March 2024) – Introduces the DUNA, proposes model legislation for adoption of the DUNA and provides a detailed analysis of the model legislation’s provisions.

***

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investments/.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.