Editor’s note: This op-ed is part of a bigger package of crypto policy views. Find the rest here: “U.S. as the crypto capital: What it would take.”

The United States benefits from what economists call the “exorbitant privilege.” As the issuer of the world’s reserve currency, it can borrow and support new spend in its own currency. However, this does not mean it can simply print money — Treasuries must still attract buyers on the open market. Fortunately, U.S. debt is widely regarded as the safest asset in the world, ensuring strong demand, particularly during times of crisis when investors rush toward safety.

Who cashes in on the exorbitant privilege? First, U.S. policymakers, who gain extra flexibility in fiscal and monetary decisions. Then, the banks — sitting at the center of global financial flows, raking in fees and influence. But the real winners? U.S. companies and multinationals, which get to do most business in their own currency, and can issue bonds and borrow more cheaply than their foreign competitors. And let’s not forget consumers, who enjoy stronger purchasing power, lower borrowing costs, and more affordable mortgages and loans.

The result? The U.S. can borrow at lower costs, sustain larger deficits for longer, and withstand economic shocks that would cripple other nations. However, the exorbitant privilege is not guaranteed — it must be earned. It depends on America’s economic, financial, and geopolitical strength. Ultimately, the entire system hinges on one crucial factor: trust. Trust in U.S. institutions, its governance, and its military. And above all, trust that, when all is said and done, the dollar remains the safest place to park global savings.

All of this has direct implications for the Trump administration’s proposed Bitcoin reserve. Proponents aren’t wrong about Bitcoin’s long-term strategic role — they’re just early. Today, the real opportunity isn’t in simply stockpiling Bitcoin; it’s in willfully shaping its integration into the global financial system in a way that reinforces U.S. economic leadership rather than undermining it. This means leveraging both USD stablecoins and Bitcoin to ensure the next era of financial infrastructure is one the U.S. leads — not one it reacts to.

Before we address that, let’s unpack the role of reserve currencies and the countries that control them.

The rise and fall of reserve currencies

History is clear: Reserve currencies belong to the world’s economic and geopolitical leaders — until they don’t. At their peak, dominant nations dictate the rules of trade, finance, and military power, providing their currency with global credibility and trust. From the Portuguese real in the 15th century to the U.S. dollar in the 20th, reserve currency issuers have shaped markets and institutions that others have followed.

But no currency holds the crown forever. Overextension — whether through war, costly expansions, or unsustainable social commitments — eventually erodes credibility. The Spanish Real de a Ocho, once backed by vast silver reserves from Latin America, declined as Spain’s mounting debts and economic mismanagement eroded its dominance. The Dutch guilder faded as relentless wars drained the Netherlands’ resources. The French franc, dominant in the 18th and early 19th centuries, weakened under the strain of revolution, Napoleonic wars, and financial mismanagement. And the British pound, once the bedrock of global finance, unraveled under the weight of post-war debts and the rise of American industrial dominance.

The lesson is simple: Economic and military power may create a reserve currency, but financial stability and institutional leadership are what sustain it. Lose that foundation, and the privilege disappears.

Is the dollar’s reign coming to an end?

The answer to that question depends on where you start the clock. The U.S. dollar solidified its status as the world’s reserve currency around World War II with the Bretton Woods Agreement, or even earlier, as the U.S. emerged as a major global creditor after World War I. Either way, the dollar has dominated for more than 80 years. By historical standards, that’s a long run, but not unprecedented — the British pound reigned for roughly a century before its decline.

Today, some argue that Pax Americana is unraveling. China’s rapid advancements in AI, robotics, electric vehicles, and advanced manufacturing signal a power shift. Adding to this, China holds significant control over the critical minerals essential to shaping our future. Other warning signs are emerging. Marc Andreessen has called DeepSeek’s R1 release an AI Sputnik moment for the U.S. — a wake-up call that U.S. leadership in emerging technologies is no longer guaranteed. Meanwhile, China’s expanding military presence — across air, sea, and cyberspace — along with its growing economic influence, raises a pressing question: Is the dollar’s dominance under threat?

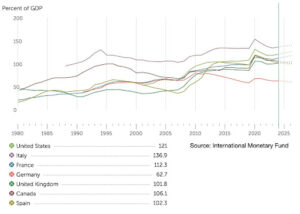

Debt as a percent of GDP. Source: International Monetary Fund

The short answer: not yet. Despite mounting debt and disinformation campaigns predicting an imminent collapse, the United States isn’t on the brink of a fiscal crisis. Yes, debt-to-GDP levels are high, particularly after pandemic spending, but they remain in line with other major economies. More importantly, global trade still overwhelmingly runs on dollars. The Chinese yuan is closing the gap with the euro in some international settlements, but it’s nowhere near to dethroning the dollar.

The real question isn’t whether the dollar will collapse. It won’t. The real concern is whether the United States can sustain its lead in innovation and economic strength. If trust in American institutions erodes or if the United States loses its competitive edge in critical industries, the cracks in dollar dominance could begin to appear. Those betting against the dollar aren’t just market speculators — they’re America’s geopolitical rivals.

That doesn’t mean fiscal discipline is irrelevant. It is extremely important. Reducing spending and improving government efficiency — through the Department of Government Efficiency (DOGE) or otherwise — would be a welcome shift. Streamlining outdated bureaucracy, clearing barriers to entrepreneurship, and fostering innovation and competition wouldn’t just cut wasteful public spending; it would also strengthen the economy and solidify the dollar’s position.

Paired with continued U.S. breakthroughs in AI, crypto, robotics, biotech, and defense technology, this approach could mirror how the U.S. regulated and commercialized the internet — fueling a new wave of economic growth and ensuring the dollar remains the world’s undisputed reserve currency.

Can a bitcoin reserve solidify U.S. financial leadership?

Enter the idea of a Bitcoin strategic reserve. Unlike traditional reserve assets, Bitcoin lacks the historical scaffolding of national institutions and geopolitical power. But that’s precisely the point. It represents a new paradigm: no national sponsor, no single point of failure, fully global, and politically neutral. Bitcoin offers an alternative that operates outside the constraints of traditional financial systems.

While many view Bitcoin as a breakthrough in computer science, its true innovation is more profound: It redefines how economic activity is coordinated and value moves across borders. By operating as a decentralized, trustless system (and one with only a pseudonymous creator who exerts no control), the Bitcoin blockchain serves as a neutral, universal ledger—an independent framework for recording global credits and debits without relying on central banks, financial institutions, political alliances, or other intermediaries. This makes it not just a technological advancement, but a structural shift in how financial coordination can function at a global scale.

That neutrality makes Bitcoin uniquely resistant to the debt crises and political entanglements that have historically unraveled fiat currencies. Unlike traditional monetary systems, which are deeply tied to national policies and geopolitical shifts, Bitcoin operates outside the control of any single government. This also gives it the potential to serve as a common economic language between nations that would otherwise resist financial integration or outright refuse a unified ledger system. The United States and China, for instance, are unlikely to trust each other’s payment rails — especially as financial sanctions become an increasingly powerful tool of economic warfare.

So how will these fractured systems interact? Bitcoin could be the bridge: a global, trust-minimized settlement layer connecting otherwise competing economic spheres. When that reality takes shape, it would undeniably make sense for the United States to hold a strategic Bitcoin reserve.

But we’re not there yet. For Bitcoin to move beyond an investment asset, critical infrastructure must be developed to ensure scalability, modern compliance frameworks, and seamless on- and off-ramps to fiat currencies for mainstream adoption.

Proponents of a Bitcoin reserve aren’t wrong about its potential long-term strategic role. They’re just early. Let’s unpack why.

Why do countries maintain strategic reserves?

Nations stockpile strategic reserves for a simple reason: In a crisis, access matters more than price. Oil is the classic example — while futures markets allow price hedging, no amount of financial engineering can substitute for having physical barrels on hand when supply chains break down due to war, geopolitics, or other disruptions.

The same logic applies to other essentials — natural gas, grains, medical supplies, and, increasingly, critical raw materials. As the world transitions to battery-driven technologies, governments are already stockpiling lithium, nickel, cobalt, and manganese to hedge against future shortages.

Then there’s currency. Countries with significant foreign debt — typically denominated in U.S. dollars — hold dollar reserves to facilitate debt rollovers and safeguard against domestic currency crises. But here’s the key difference: no nation currently carries significant liabilities in Bitcoin — at least not yet.

Bitcoin proponents argue that its long-term price trajectory makes it an obvious reserve asset. If the United States buys in now and adoption continues, the investment could multiply in value. However, this approach aligns more with the strategy of a sovereign wealth fund, which focuses on capital returns, rather than that of a reserve critical to national security. It is a better fit for resource-rich but economically imbalanced nations looking for an asymmetric financial windfall or countries with weak central banks hoping Bitcoin can stabilize their balance sheets.

So where does that leave the United States? It doesn’t need Bitcoin to run its economy just yet, and although President Trump recently announced the establishment of a sovereign wealth fund, crypto investments may still (rightly) be left primarily to private markets for efficient allocation. The strongest case for a Bitcoin reserve is not one of economic necessity but of strategic positioning. Holding a reserve could signal that the United States is making a decisive bet to lead in crypto, establish clear regulatory frameworks, and position itself as the global hub for DeFi, much like it has dominated traditional finance for decades. However, at this stage, the costs of such a move could outweigh the benefits.

Why a Bitcoin reserve could backfire

Beyond the logistical challenges of accumulating and securing a Bitcoin reserve, the bigger issue is perception, and the cost could be significant. In the worst case, it could signal a lack of confidence in the U.S. government’s ability to sustain its debt, a strategic misstep that would hand a victory to geopolitical rivals like Russia and China, both of whom have long sought to weaken the dollar.

Russia hasn’t just promoted de-dollarization abroad; its state-backed media has spent years pushing narratives that question the stability of the U.S. dollar and that predict its imminent decline. China, meanwhile, has taken a more direct approach, expanding the yuan’s reach and digital payment infrastructure — including through the domestically focused digital renminbi — as a challenger to the U.S.-led financial system, particularly in cross-border trade and payments. And in global finance, perception matters. Expectations don’t just reflect reality; they help shape it.

If the U.S. government began accumulating Bitcoin at scale, markets could interpret it as a hedge against the dollar itself. This perception alone could potentially trigger investors to sell dollars or reallocate capital, undermining the very position the U.S. aims to protect. In global finance, belief drives behavior. If enough investors start doubting the dollar’s stability, their collective actions would turn that doubt into reality.

U.S. monetary policy relies on the Federal Reserve’s ability to manage interest rates and inflation. Holding a Bitcoin reserve could send a contradictory message: If the government is confident in its own economic tools, why stockpile an asset beyond the Fed’s control?

Would a Bitcoin reserve alone trigger a U.S. dollar crisis? Highly unlikely. But it also may not strengthen the system either — and in geopolitics and finance, unforced errors are often the most expensive.

Leading with strategy, not speculation

The best way for the U.S. to lower its debt-to-GDP ratio isn’t through speculation, it’s through fiscal discipline and economic growth. History is clear: Reserve currencies don’t last forever, and those that fall do so from economic mismanagement and overextension. To avoid joining the fate of the Spanish real de a ocho, the Dutch guilder, the French livre, and the British pound, the United States must focus on sustainable economic strength, not risky financial bets.

If Bitcoin were to become the global reserve currency, the U.S. would have the most to lose. There is no smooth transition from dollar dominance to a Bitcoin-based system. Some argue that Bitcoin’s appreciation could help the United States “repay” its debt, but the reality would be far harsher. Such a shift would make it exponentially more difficult for the United States to finance its obligations and sustain its economic influence.

And while many dismiss the idea of Bitcoin ever becoming a true medium of exchange and unit of account, history suggests otherwise. Gold and silver weren’t just valuable because they were scarce, they were also divisible, durable, and portable, making them effective currencies — even without sovereign backing or issuance, much like Bitcoin today. Similarly, China’s early paper money didn’t begin as a government-imposed medium of exchange. It evolved from commercial promissory notes and deposit certificates — representations of already trusted stores of value — before gaining wider acceptance as a medium of exchange.

Fiat currencies are often seen as an exception to this pattern — declared legal tender by the government, they function immediately as a medium of exchange and later as a store of value. But this oversimplifies reality. What gives fiat money its strength isn’t just legal decree, it’s the government’s ability to enforce taxation and its capacity to meet debt obligations through this power. A currency backed by a state with a strong tax base has intrinsic demand because businesses and individuals need it to settle obligations. This taxation power is what enables fiat currencies to retain value, even without a direct commodity backing.

But even fiat systems weren’t built from scratch. Historically, their credibility was bootstrapped from commodities people already trusted, most notably gold. Paper money gained acceptance precisely because it was once redeemable for gold or silver. The transition to pure fiat only became viable after decades of that trust being reinforced.

Bitcoin is following a similar trajectory. Today, it is primarily seen as a store of value — volatile, yet increasingly regarded as digital gold. However, as adoption expands and financial infrastructure matures, its role as a medium of exchange will likely follow. History suggests that once an asset is widely recognized as a reliable store of value, the transition to a functioning currency is a natural progression.

For the U.S., this presents a major challenge. While some policy levers exist, Bitcoin operates largely outside the traditional controls countries have over money. If it gains traction as a global medium of exchange, the U.S. will face a stark reality — reserve currency status is not easily relinquished or shared.

That doesn’t mean the U.S. should fight or ignore Bitcoin — if anything, it should actively engage with and shape its role in the financial system. But simply buying and holding it for price appreciation isn’t the answer either. The real opportunity is greater—but also more challenging: driving Bitcoin’s integration into the global financial system in a way that strengthens U.S. economic leadership rather than eroding it.

A Bitcoin platform play for the United States

Bitcoin is the most established cryptocurrency, with an unmatched track record in security and decentralization. This positions it as the strongest candidate for mainstream adoption, first as a store of value and, eventually, as a medium of exchange.

For many, Bitcoin’s appeal lies in its decentralized nature and scarcity—factors that propel its price as adoption accelerates. But that’s a narrow view. While Bitcoin will continue to gain value as it diffuses, the real long-term opportunity for the U.S. isn’t just in holding it — but in actively shaping its integration into the global financial system and establishing itself as the international hub for Bitcoin finance.

For every country except the United States, simply buying and holding Bitcoin is a perfectly viable strategy — one that accelerates its adoption while capturing financial upside. But the U.S. has far more at stake and must do more. It needs a different approach — one that not only preserves its role as the issuer of the world’s reserve currency, but also drives large-scale financial innovation on the U.S. dollar “platform.”

The key precedent here is the internet, which transformed the economy by moving information exchange from proprietary networks to open ones. Today, the U.S. government faces a similar choice as pre-internet incumbents, as financial rails shift toward a more open and decentralized infrastructure. Just as companies that embraced the internet’s open architecture thrived while those that resisted eventually became irrelevant, the U.S.’s approach to this transition will determine whether it retains its global financial influence or cedes ground to others.

The first pillar of a more ambitious, future-proof strategy is to embrace Bitcoin as a network, not just as an asset. As open, permissionless networks drive the new financial infrastructure, incumbents must be willing to relinquish some control. By doing so, however, the U.S. can unlock significant new opportunities. History shows that those who adapt to disruptive technologies strengthen their position, while those who resist ultimately lose out.

A second key pillar that complements Bitcoin is accelerating the adoption of USD stablecoins. With proper regulation, stablecoins can reinforce the public-private partnership that has underpinned U.S. financial dominance for over a century. Rather than weakening dollar supremacy, stablecoins can bolster it, expanding the USD’s reach, enhancing its utility, and securing its relevance in a digital economy. Moreover, they offer a far more agile and flexible solution than slow-moving, bureaucratic central bank digital currencies or ill-defined unified ledger proposals like the Bank for International Settlements’ “Finternet.”

But not every country will want to adopt USD stablecoins or operate entirely within the U.S. regulatory framework. This is where Bitcoin plays a critical strategic role — serving as a bridge between the core USD platform and non-geopolitically aligned economies. In this context, Bitcoin could serve as a neutral network and asset that facilitates financial flows while reinforcing the U.S.’s central role in global finance, thereby preventing it from ceding ground to alternatives like the yuan. Even if it serves as a pressure release valve for nations seeking alternatives to dollar hegemony, Bitcoin’s decentralized, open nature ensures that it aligns more closely with U.S. economic and social values than with those of authoritarian regimes.

If the U.S. successfully executes this strategy, it will become the epicenter of Bitcoin financial activity, giving it greater influence to shape those flows in line with U.S. interests and principles.

This is a delicate yet viable strategy that, if executed effectively, could extend the U.S. dollar’s relevance for decades. Rather than simply stockpiling Bitcoin reserves, which could signal doubt in the dollar’s stability, strategically integrating Bitcoin into the financial system to advance both the dollar and USD stablecoins on the network positions the U.S. government as an active steward rather than a passive observer.

The upside? A more open financial infrastructure where the U.S. still controls the “killer app” — the U.S. dollar. This approach mirrors what companies like Meta and DeepSeek do by open-sourcing their AI models to set industry standards while monetizing elsewhere. For the U.S., it means expanding the USD platform and making it interoperable with Bitcoin, ensuring continued relevance in a future where cryptocurrencies play a central role.

Of course, as with any bet against disruption, this strategy carries risks. But the cost of resisting innovation is obsolescence. If any administration can pull this off, it’s the current one — with deep expertise in platform wars and a clear understanding that staying ahead isn’t about controlling an entire ecosystem, but about shaping how value is captured within it.

***

Christian Catalini is the co-founder of Lightspark and the MIT Cryptoeconomics Lab.

***

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the current or enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.