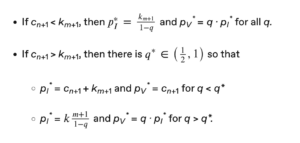

We have characterized the optimal mechanism for incentivizing informed voting by paying people to vote with a majority. Three features of this mechanism highlight some real concerns with the feasibility of actually implementing such incentives.

The first is that providing the right incentives can be quite expensive. In our example, the total cost of voting and information borne by token holders is $23 (token holders 1 and 2 bear the costs of voting and information, token holder 3 only bears the cost of voting). Yet total compensation paid out by the mechanism is $71.5 (token holders 1 and 2 each receive $27.5 while token holder 3 receives $16.5). Unfortunately, because the platform doesn’t know the voters’ costs, there isn’t a cheaper way to achieve the goal.

More generally, the total cost of inducing m informed votes and n total votes is

Total Cost = m · pI* + (n – m) · pV*.

This total cost depends on three things:

- The number of votes and informed votes that need to be purchased (m and n – m),

- The token holders’ costs of voting and information (cn+1 and km+1), and

- How much uncertainty there is about the correct choice (q).

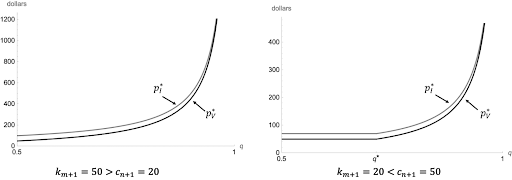

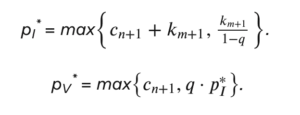

The platform’s costs are increasing linearly in m, n – m, cn+1, and km+1. But as Figure 4 illustrates, they are increasing hyperbolically in q. Moreover, as q gets close to 1, so there is essentially no uncertainty about the correct choice, the cost of inducing informed voting goes to infinity. This is because, if A is almost certain to be the correct option, there is no reason for token holders in group I to invest in becoming informed. They can just vote A and almost certainly be in the majority anyway. Thus, it is probably only feasible to consider buying informed votes when there is substantial uncertainty about the correct choice – that is, when q is close to one-half. Fortunately, this is also presumably the circumstance where informed voting is most valuable.

A second concern is that the mechanism may be somewhat difficult for token holders to understand — although the requirements of the token holders may be less taxing than the mathematics suggest. Token holders need to be able to (1) state their own personal costs of voting and of getting information and (2) upon being given a simple contract, be able to understand the direction of their monetary incentives.

The third concern is more fundamental. Any incentive scheme that works based on whether voters vote with the majority in their group is subject to concerns about coordination problems. That is, the analysis above shows that it is an equilibrium for all token holders to behave as described. But there is always another equilibrium.

Imagine a token holder in group I believes that no other token holder in group I is going to invest in information. Then that token holder believes that knowing the right option will not help them vote with the majority of group I, since the majority vote will not be determined by what the right option is. As such, that token holder has no incentive to invest in information. Thus, under an incentive scheme that pays people to vote with the majority of group I, in addition to the good “informed” equilibrium, there is also always a bad “uninformed” equilibrium in which no token holder invests in information because they (correctly) believe other token holders won’t invest in information.

***

Our takeaway from these analyses is that rewarding or slashing voters based on whether they vote in the majority or minority is not the most promising way to reward voting while discouraging uninformed voting or bot voting.

For projects that think the basic rewards mechanism is too vulnerable to gaming or uninformed voting, a logical way to start is by only offering rewards to addresses with some kind of track record of contributions to the project. This would be in line with recent experiments in retroactive rewards, such as Optimism’s ongoing work.

Separately or in addition, projects could also explore staking requirements that only provide rewards to addresses that are locked into the protocol for long periods of time, to disincentivize short-term voting rewards harvesting.

***

Ethan Bueno de Mesquita is the Sydney Stein Professor at the Harris School of Public Policy at the University of Chicago. His research focuses on applications of game theoretic models to a variety of political phenomena. He advises tech companies and others on governance and related issues.

Andrew Hall is a Professor of Political Economy in the Graduate School of Business at Stanford University and a Professor of Political Science. He works with the a16z research lab and is an advisor to tech companies, startups, and blockchain protocols on issues at the intersection of technology, governance, and society.

***

Editor: Tim Sullivan

***